Every year, WalktheChat compiles the best data from digital luxury analysts into one report packed with insights.

This year we combined data from McKinsey, Bain, BCG and Tencent in order to give you a snapshot of the Chinese Digital Luxury market as of 2019.

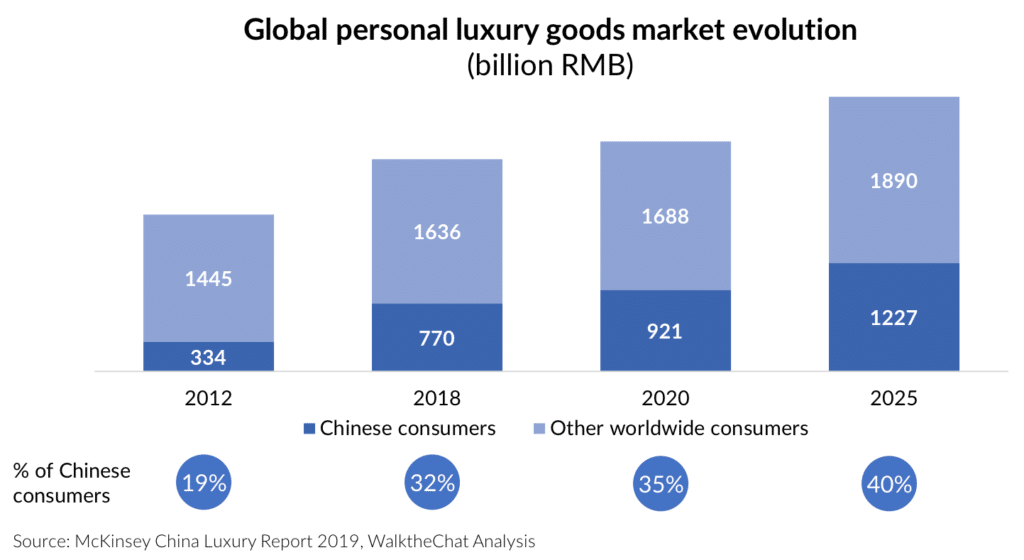

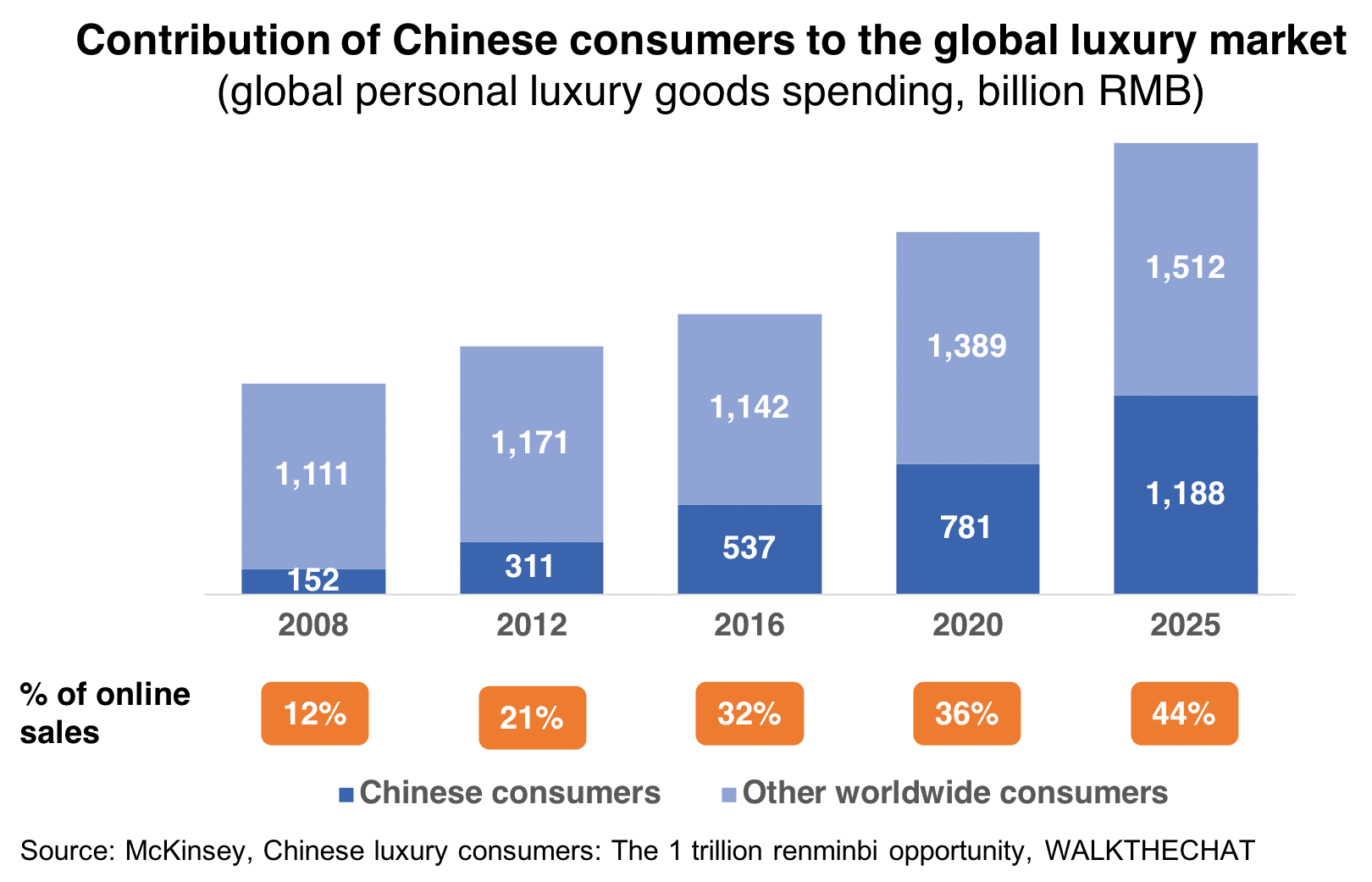

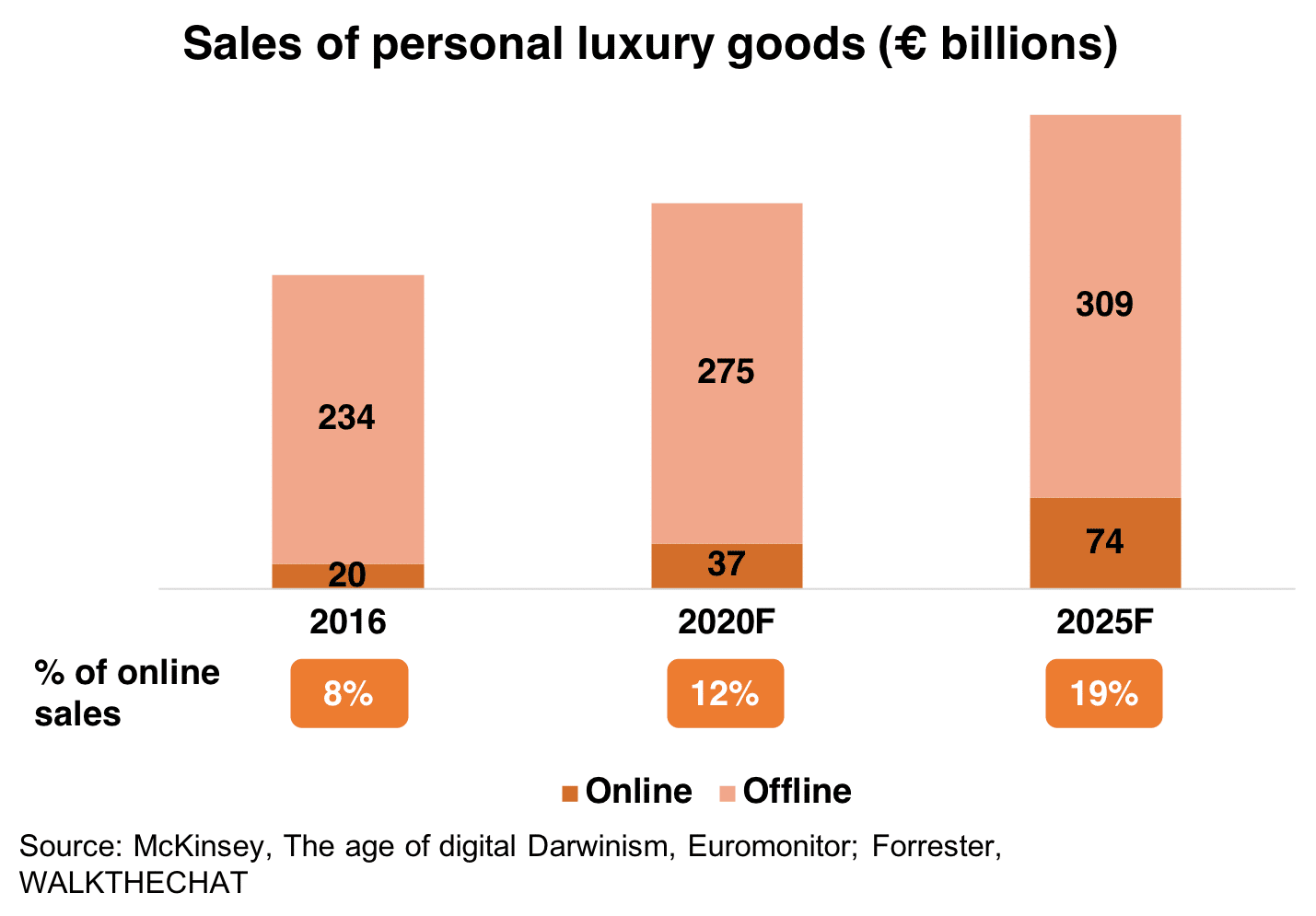

The global personal luxury goods market is expected to grow from 2,406 billion RMB in 2018 to 3,117 billion RMB in 2025 (a roughly 4% annual growth rate)

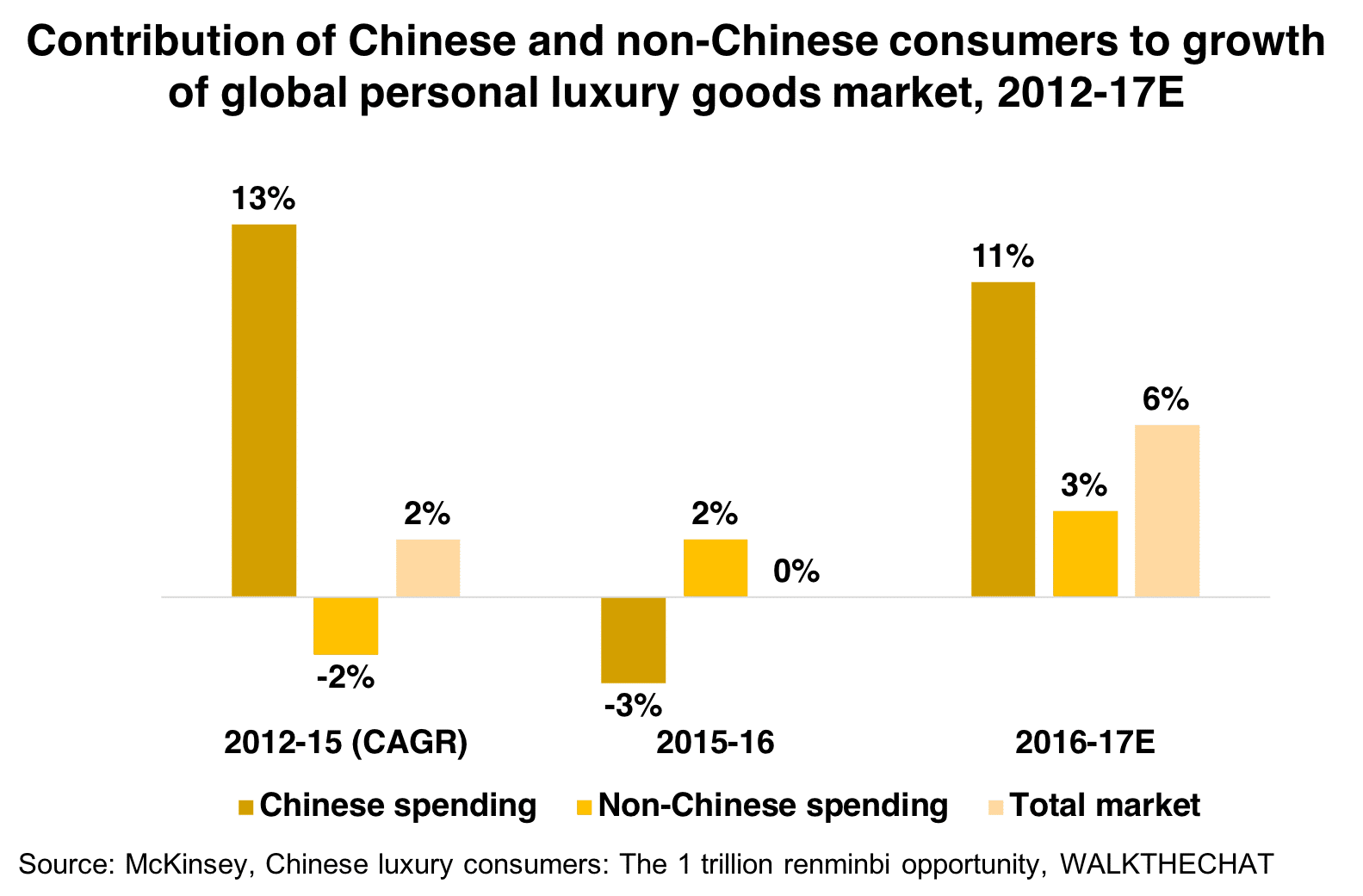

The luxury market in 2025 will, however, be significantly different from what it was in 2012. According to McKinsey, the percentage of purchases from Chinese customers will have doubled from 19% to 40% of the personal luxury goods market.

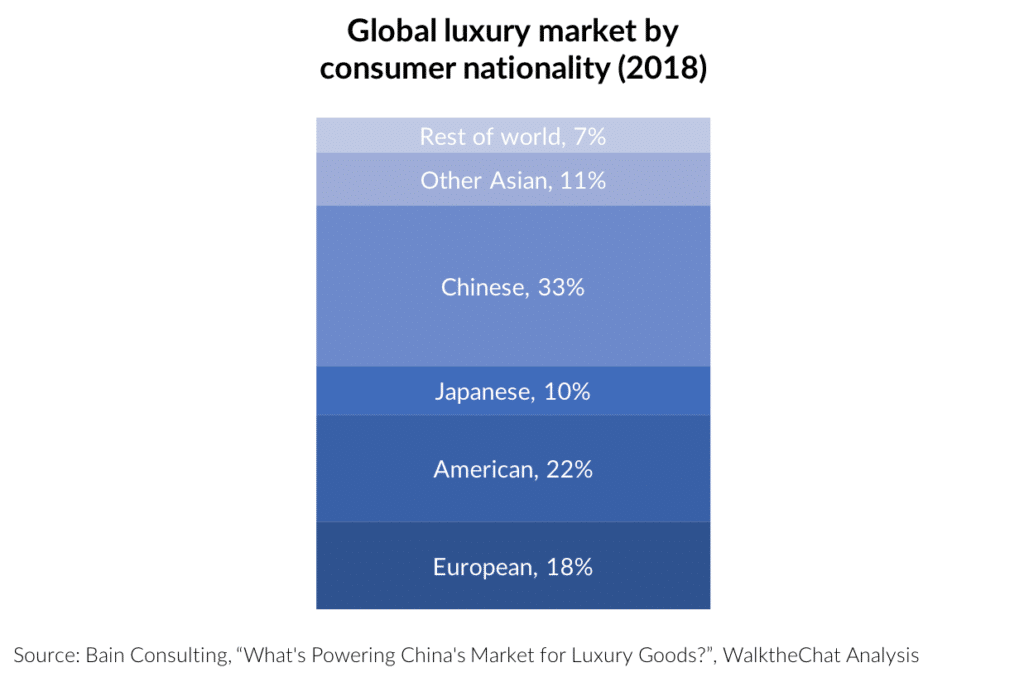

These estimates closely match the data obtained by other consulting companies. According to Bain Consulting, Chinese customers make up 33% of global luxury purchases as of 2018.

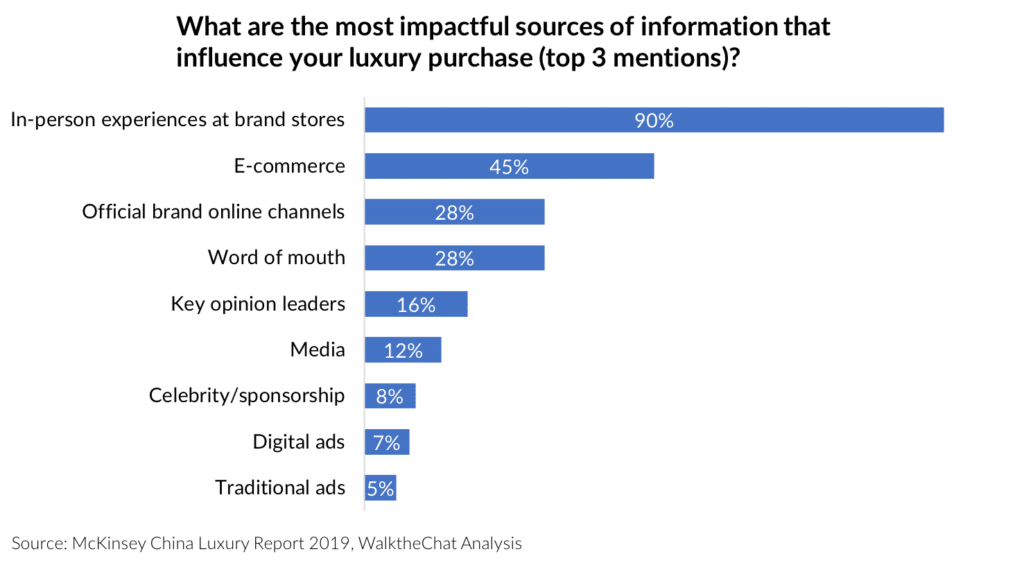

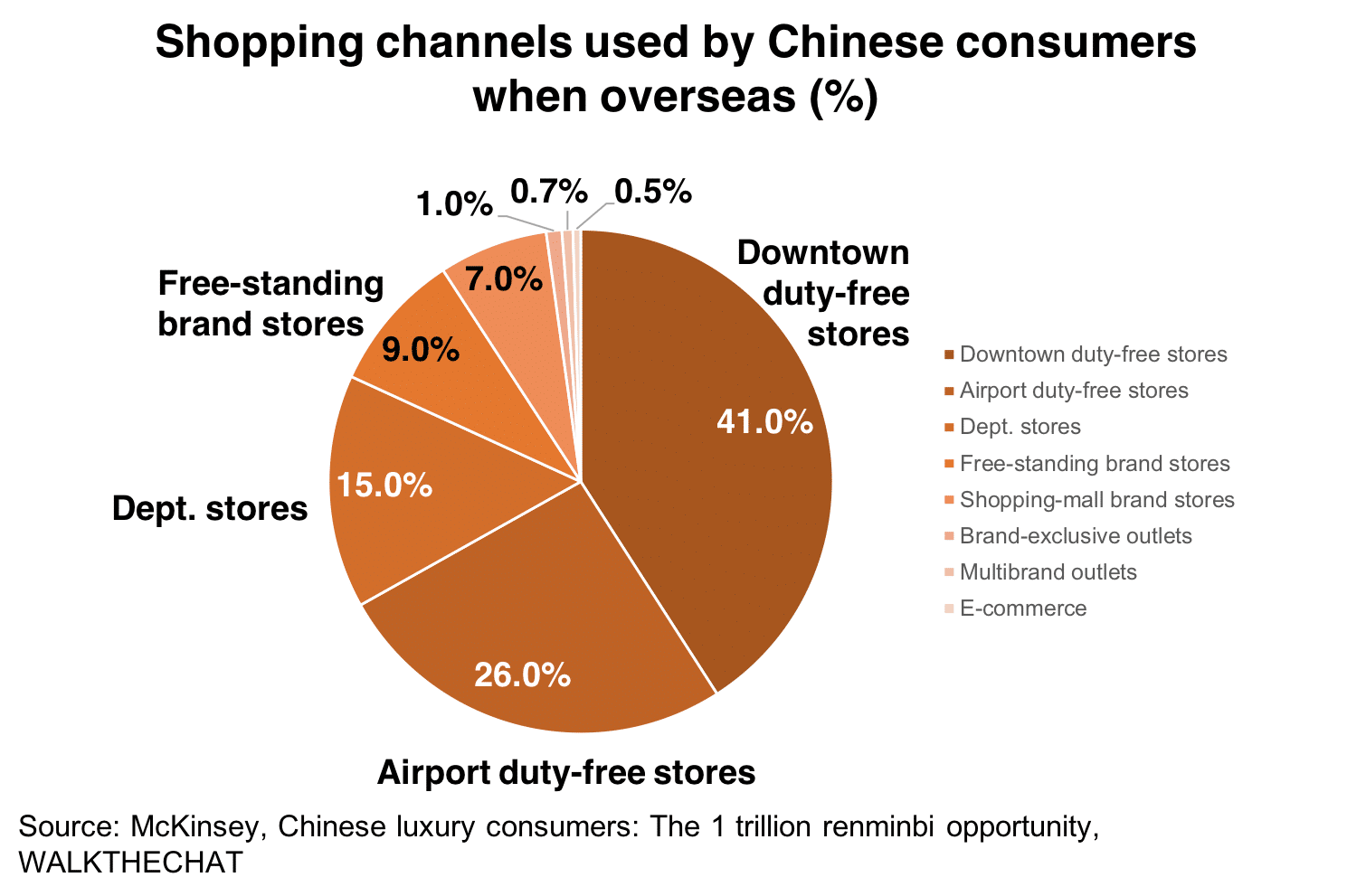

The luxury market remains very centered around offline experience. In a McKinsey survey, offline store experience is the most frequently mentioned source of information for luxury buyers.

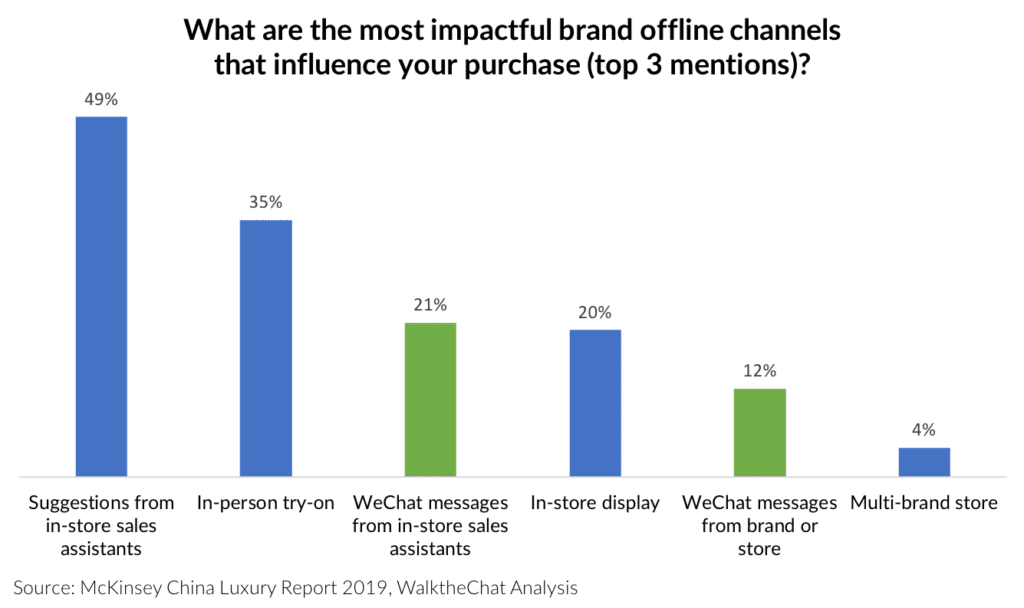

Customers however mention that WeChat messages from the store or salesperson are an important driver of their purchasing decisions.

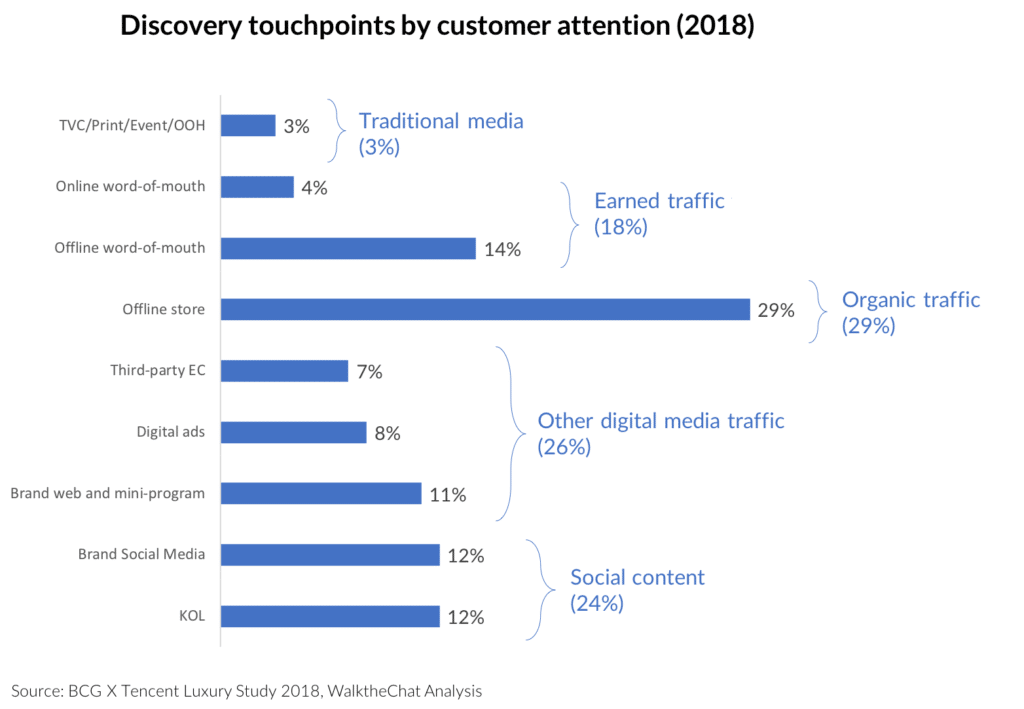

Although offline stores are an important influence on the final purchasing decision, digital marketing plays a crucial role in the discovery of new brands.

According to a joint study by BCG and Tencent, 54% of the discovery touchpoints happen online: either via social media, other digital channels, or online word-of-mouth.

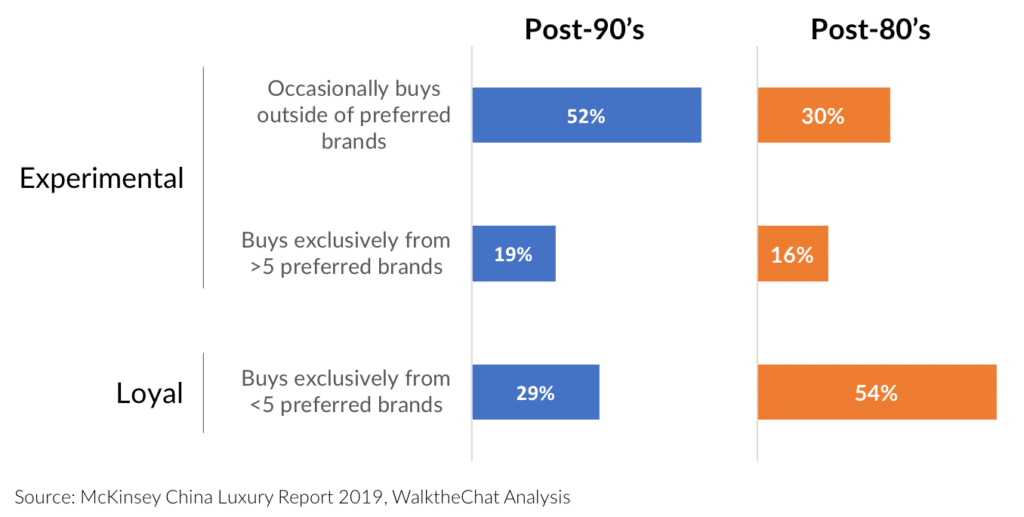

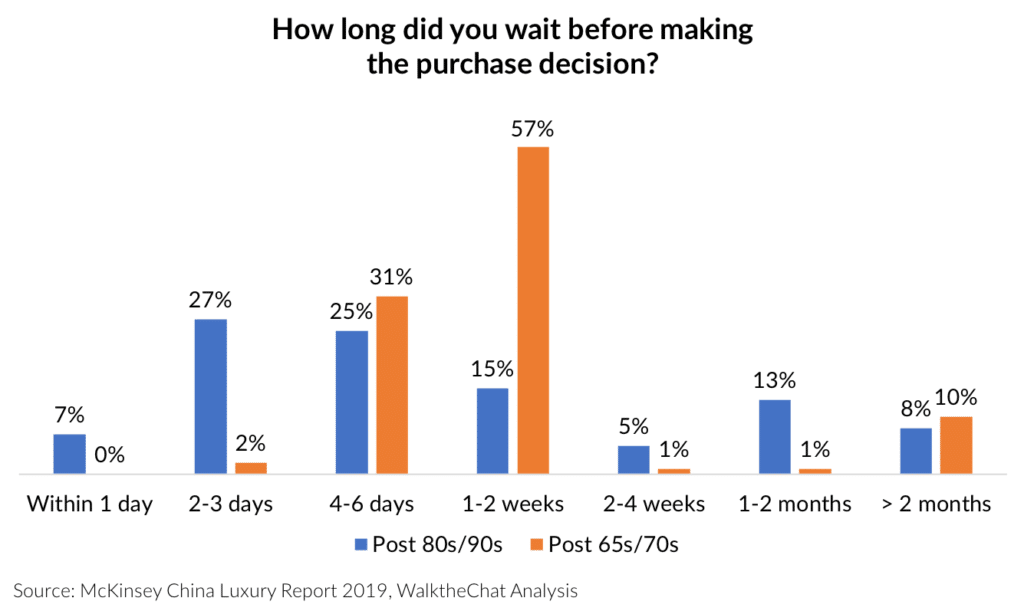

The way consumers discover brands also depends on their age. The post-90s generations are much more likely to be experimental and go for up-and-coming brands, while older generations are loyal to a few brands they keep buying from.

Younger customers are also much more likely to engage in impulse purchases. 34% of 80s/90s generations will make their purchasing decisions in less than 3 days, against only 2% of post 65s/70s generation.

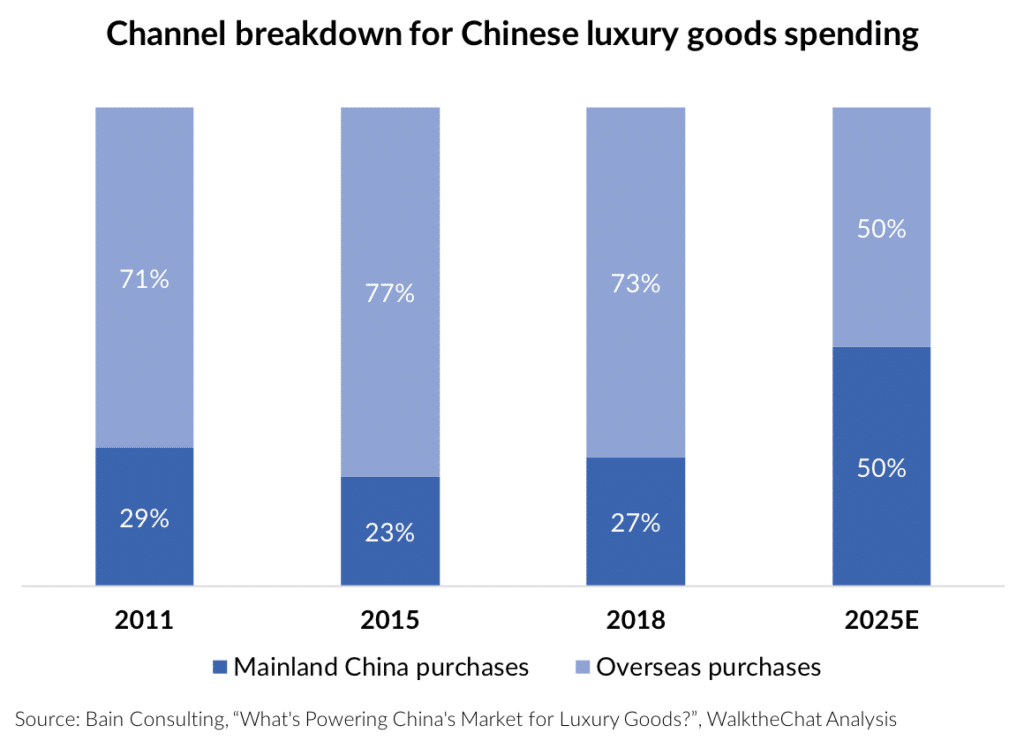

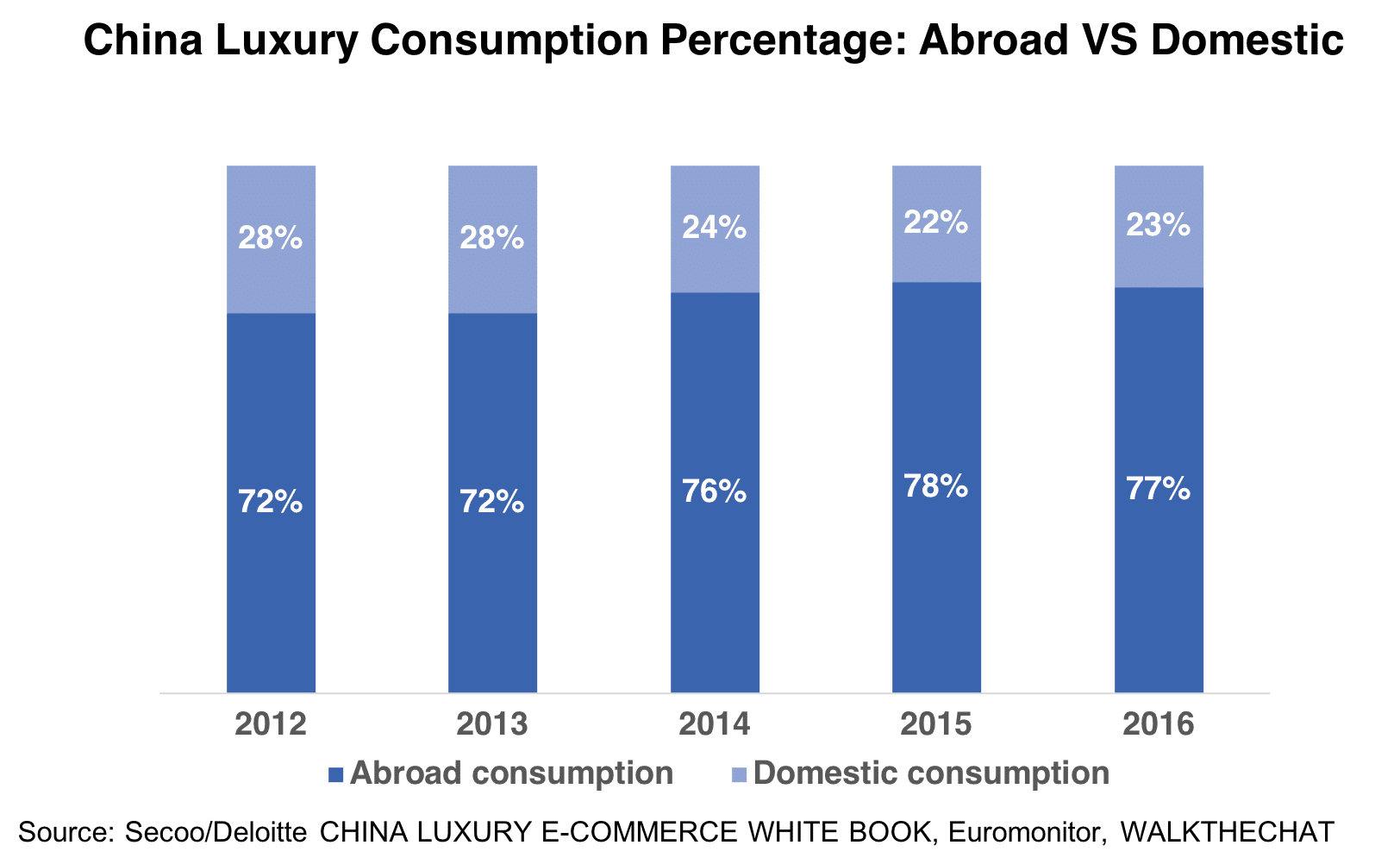

A strong tendency is the shift of Chinese customers to buy luxury products mostly from Mainland China.

This is mostly due to the reduction in import duty, the crackdown on gray markets (Daigou resellers on Taobao) and the price harmonization between Mainland China and abroad.

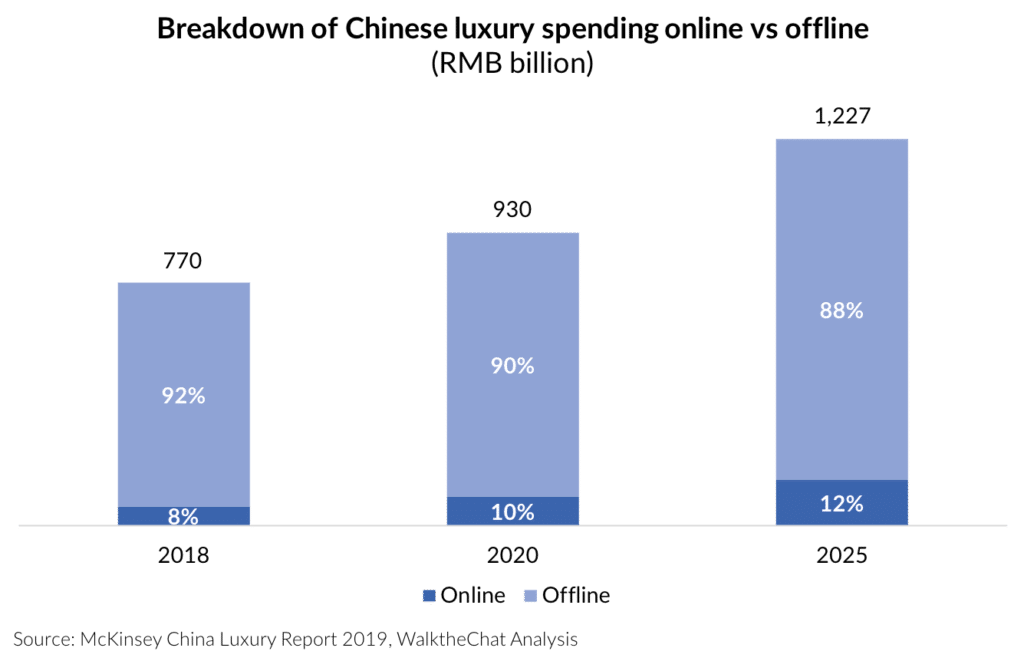

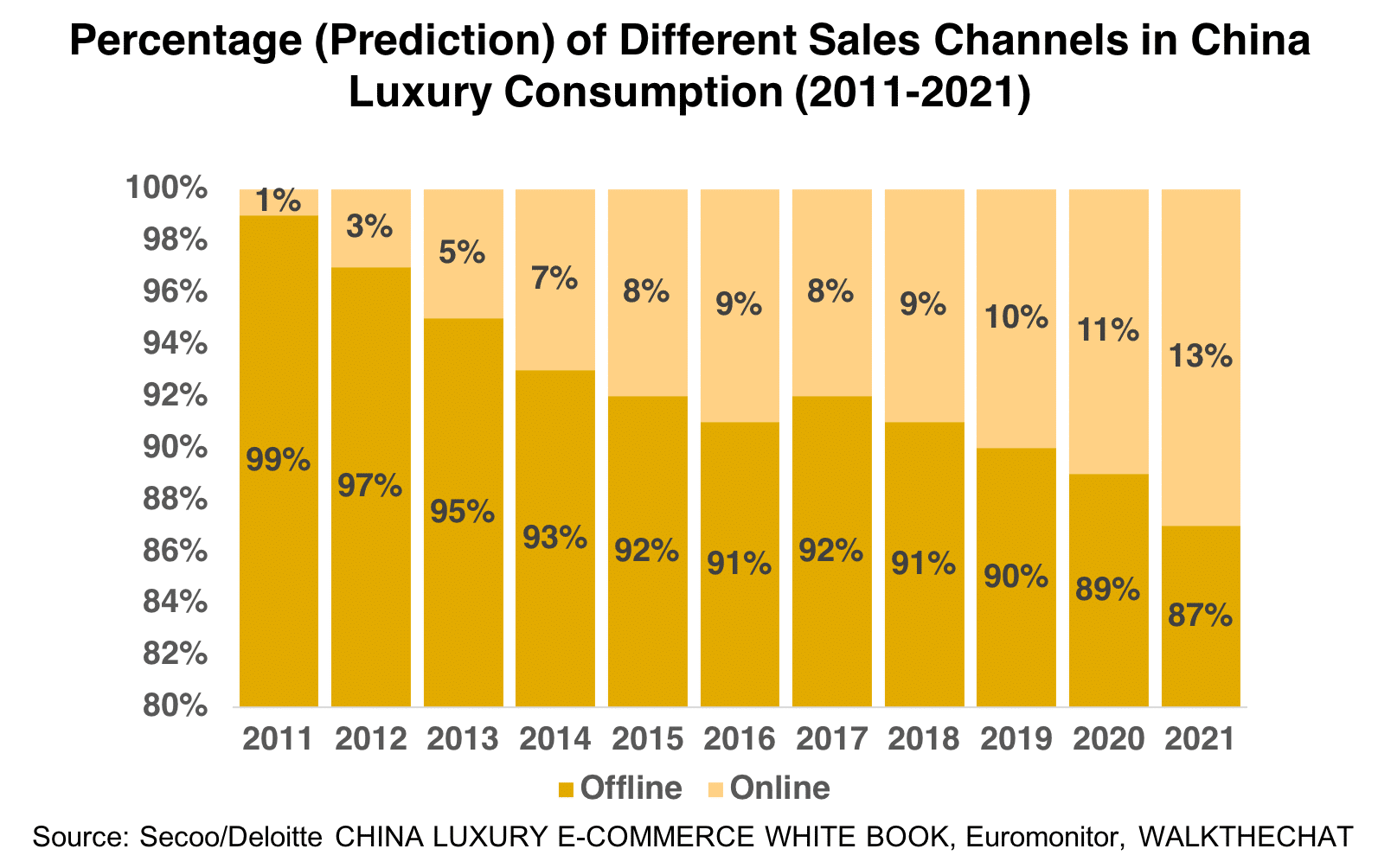

As we mentioned previously, the Chinese luxury market is still mostly an offline market. The share of online sales in the Chinese luxury market is however expanding to grow from 8% to 12% by 2025.

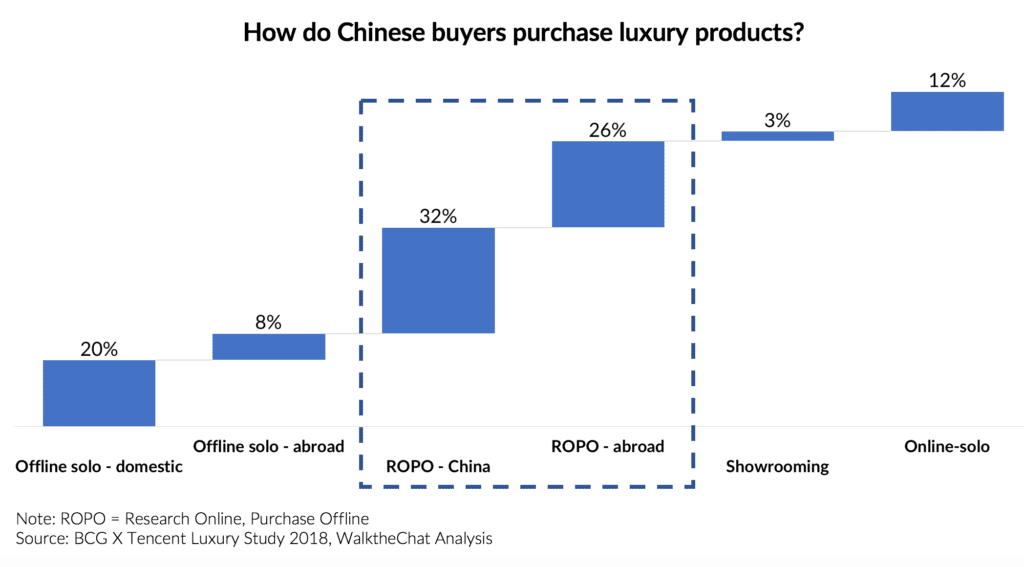

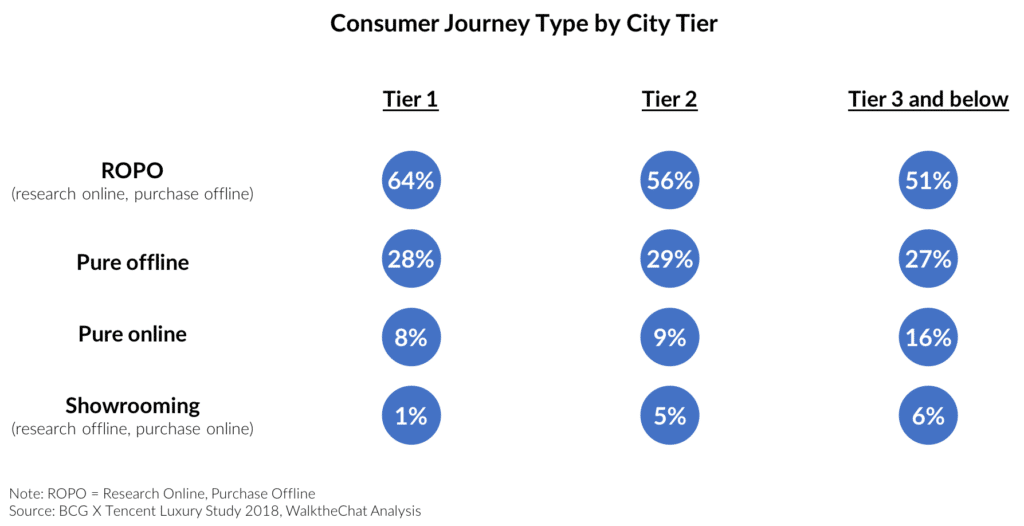

However, purchasing behaviors are more complex: according to the BCG x Tencent report, 58% of luxury buyers purchase offline after having researched products online, while only 28% make purchases solely based on offline information.

This concept of online research to buy in offline stores is abbreviated as ROPO (Research Online, Purchase Offline) which is the opposite of showrooming (Research Offline, Purchase Online).

This behavior also varies based on the location of Chinese consumers.

Although pure online purchases and showrooming make up for only 9% of purchases in Tier 1 cities, they amount to 22% of luxury purchases in Tier 3 cities and below (where there is also less access to offline locations).

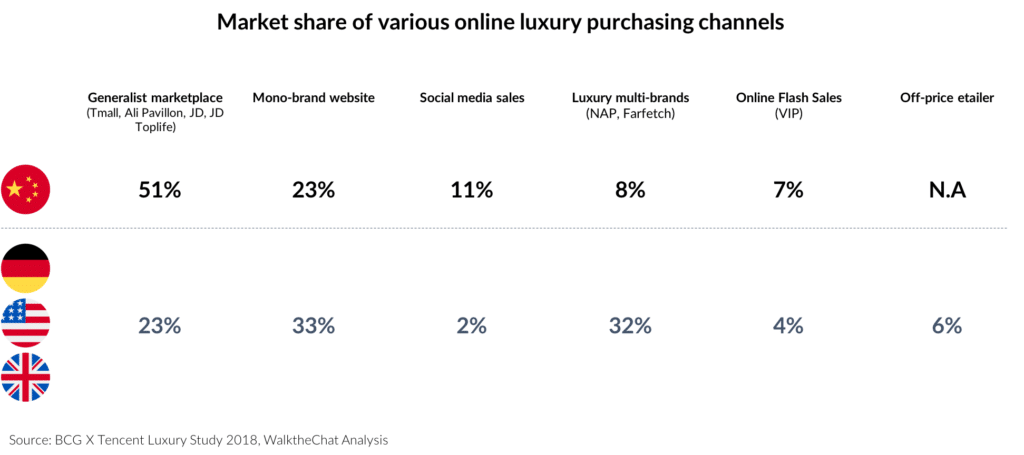

In terms of purchasing channels, Chinese luxury buyers differ radically from their Western counterparts.

Chinese customers are much more likely to buy luxury products on generalist marketplaces such as Tmall or JD (51% in China against 23% in the West) and much less likely to go through luxury multi-brands websites such as Net-a-Porter or Farfetch (8% in China against 32% in the West). Social media is also the 3rd largest sales channel for Chinese consumers making up 11%, against only 2% in the West.

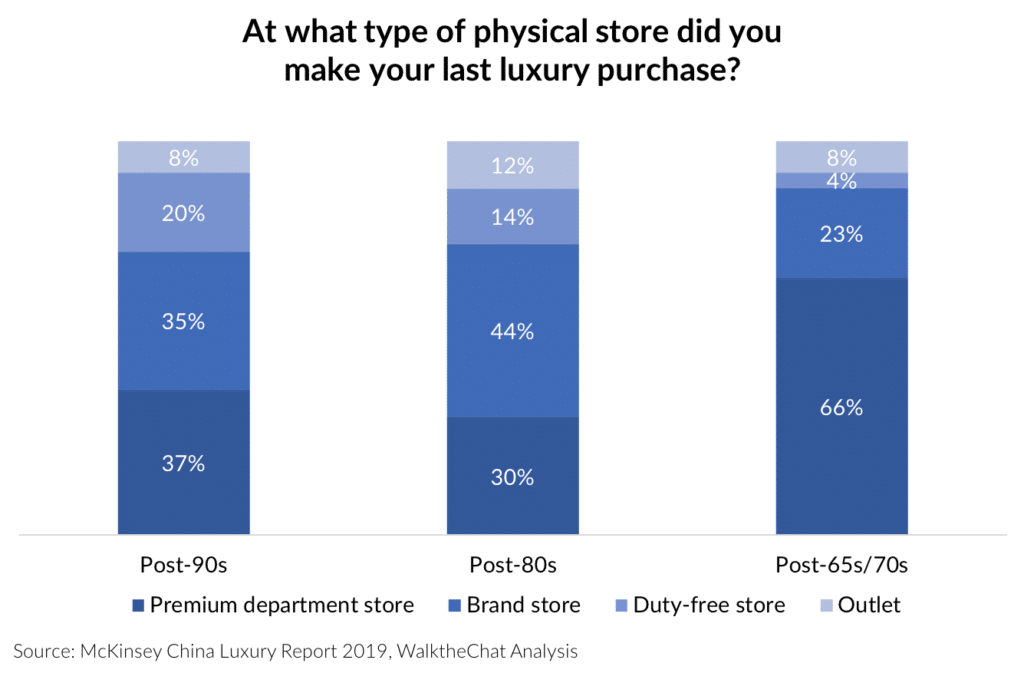

When it comes to offline purchases, post-90s also differ from older generations. They are much less likely to purchase from premium department stores such as Galeries Lafayette (37% of post-90s against 66% of post-65s/70s)

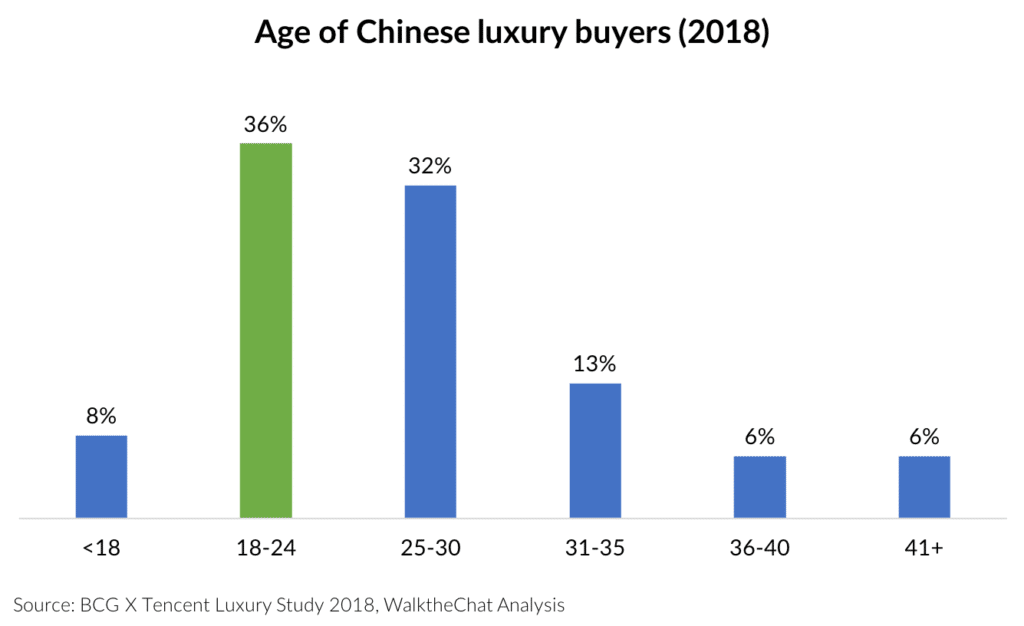

Chinese luxury buyers are relatively young: 36% of them are between 18 and 24 years old.

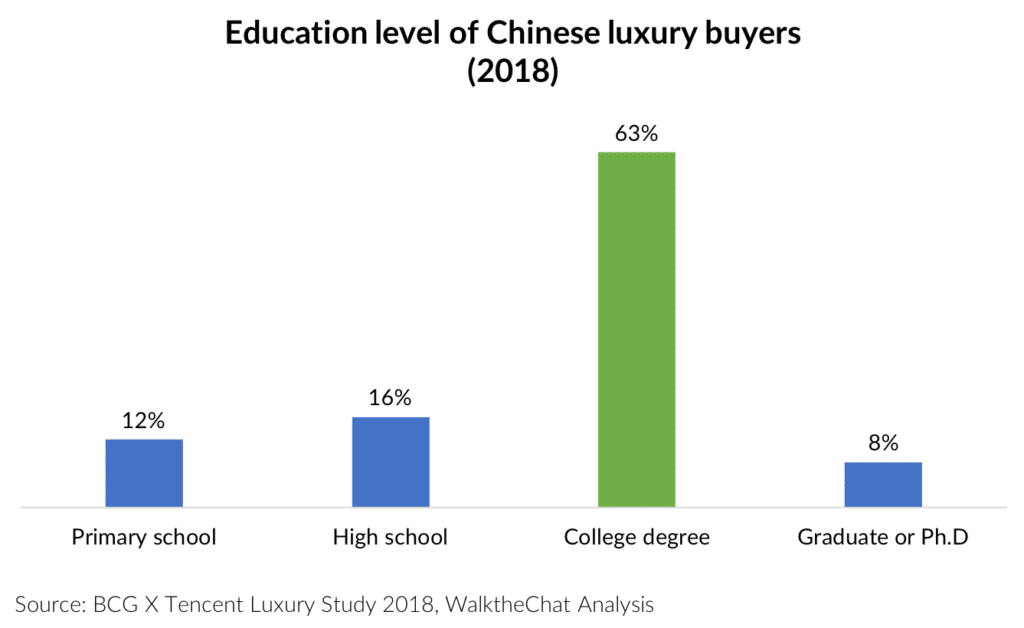

They are also very educated, with 71% of them holding at least a college degree.

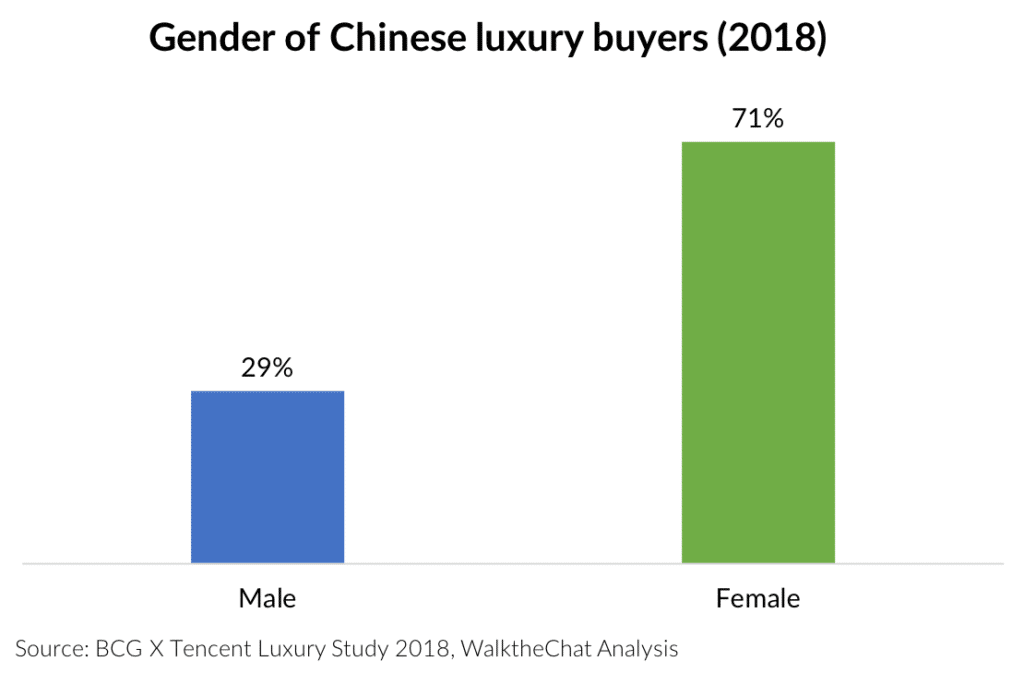

Chinese luxury buyers are also overwhelmingly female: 71% of them are women.

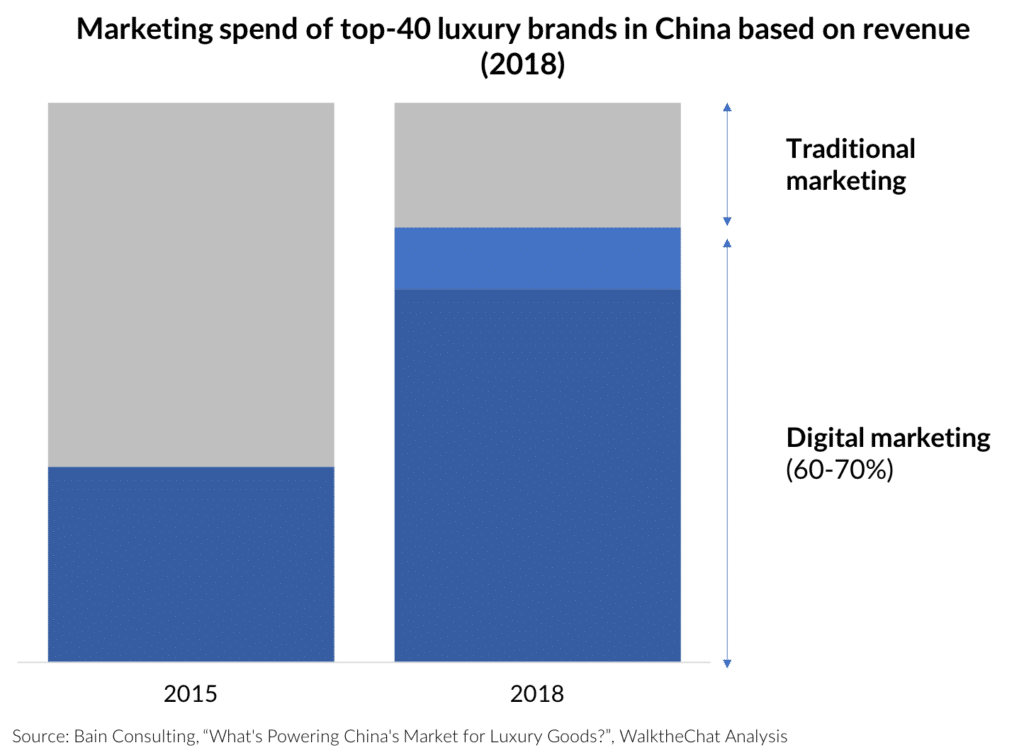

The marketing budget of luxury brands has brutally shifted over the last few years. From 2015 to 2018, the proportion of the marketing budget of luxury brands dedicated to digital went from 35% to 60-70%.

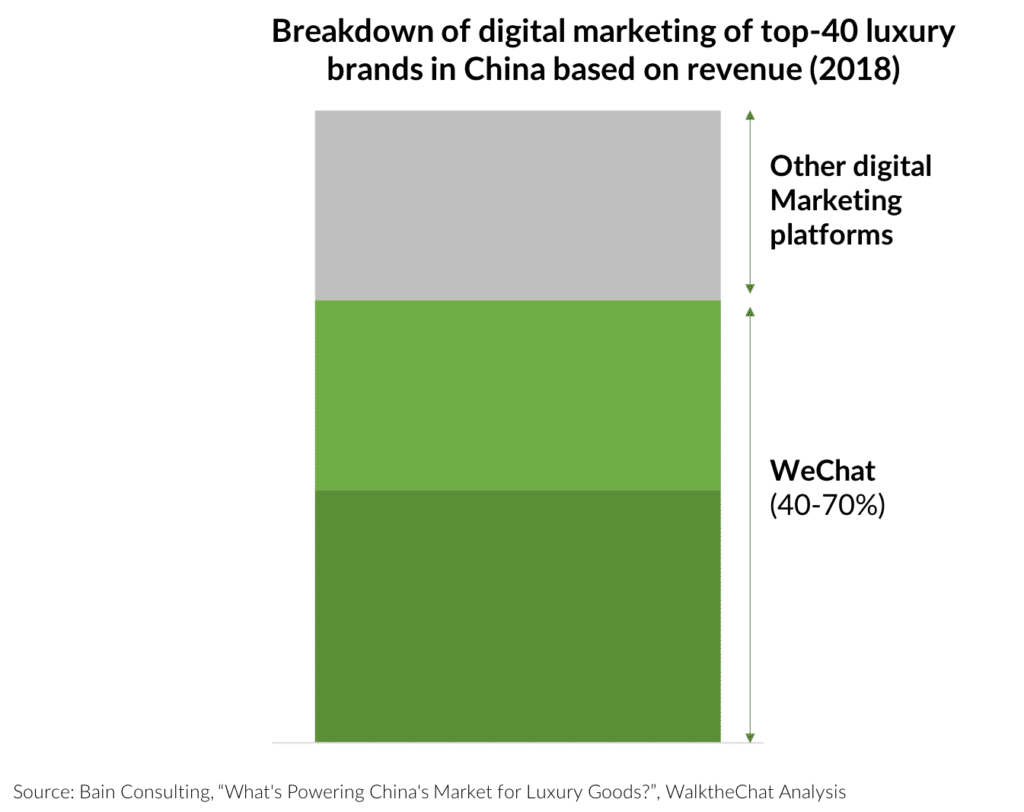

Most of this budget went to WeChat, which amounts for 40-70% of the digital marketing budget of luxury brands.

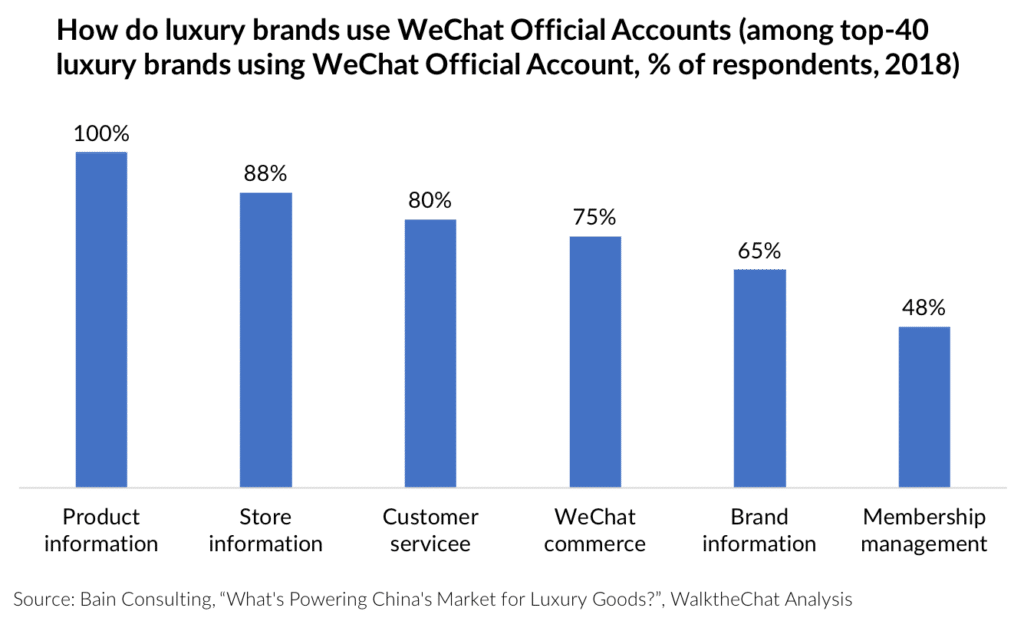

All of the top-40 luxury brands who use WeChat leveraged the platform to share product information, while already 75% of them used the messaging platform for e-commerce purposes.

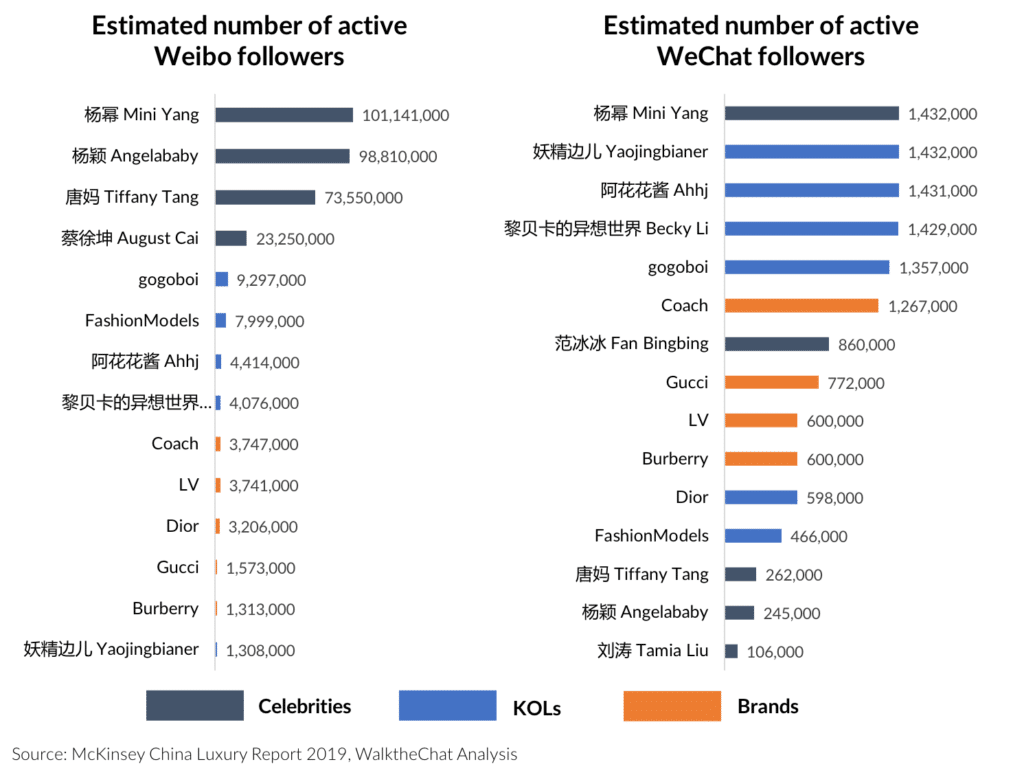

Brands are however far from catching up with KOLs and superstars in terms of online audiences.

This leads to fruitful collaborations between luxury brands and KOLs, where brands can benefit from the influencers reach, and leverage the personal connection with the audience in order to help convey the brand’s message.

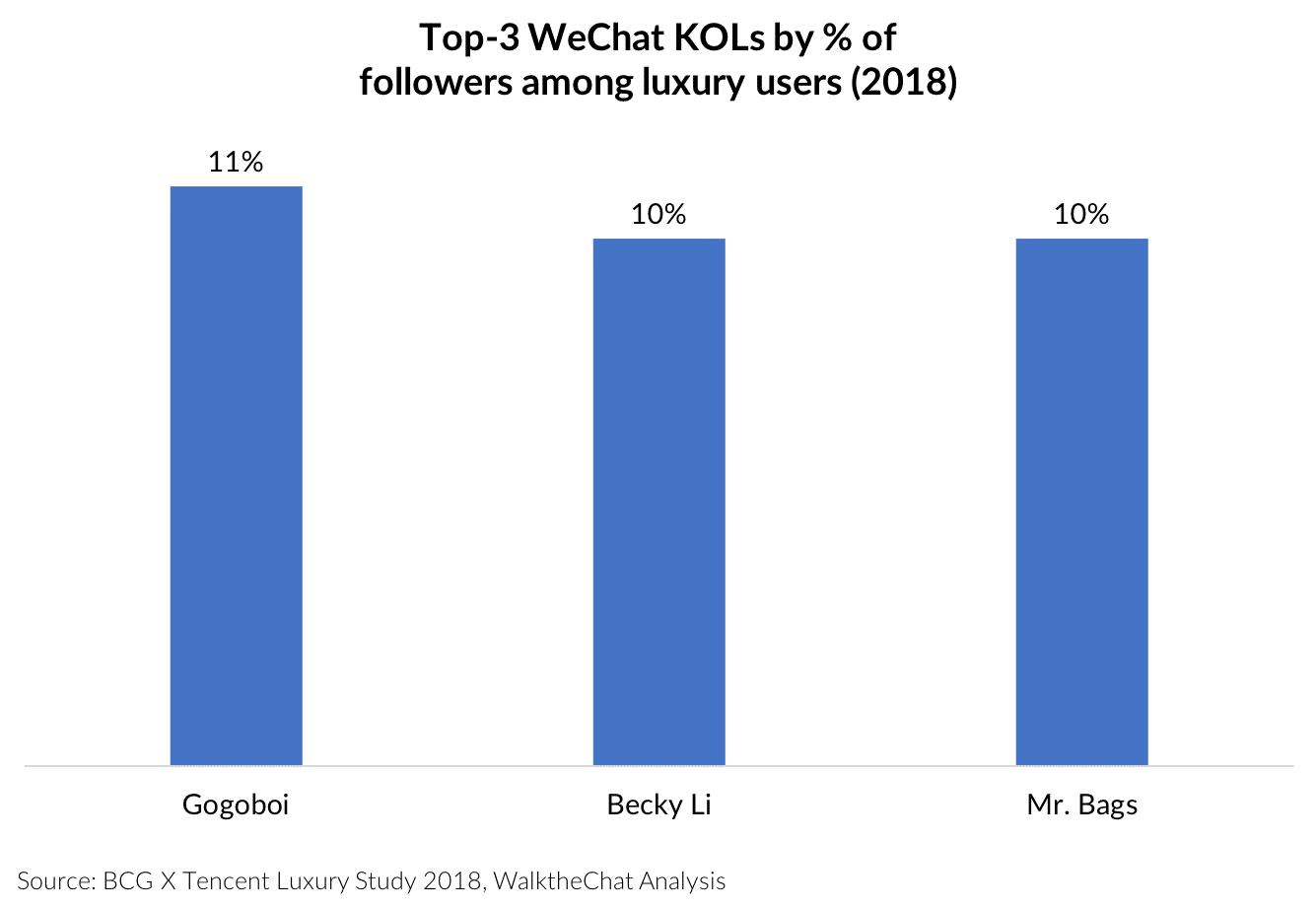

Yet, not all influencers have audiences that are relevant to luxury brands.

In fact, the top-3 influencers in terms of luxury consumer audience only have 10% to 11% of their followers actually purchasing luxury products.

Conclusion

The Chinese luxury market is currently undergoing major shifts, from the migration of customers from offline to online (especially in smaller cities) to the increasing percentage of consumers buying directly from mainland China.

Although this data can seem abstract, it is nonetheless essential in order for brands to understand who are their target customers and what they want.

Quantitative data, combined with practical operational insights, is essential in order to craft a relevant marketing and distribution strategy in the fast-moving Chinese luxury market.

China Digital Luxury Report 2018

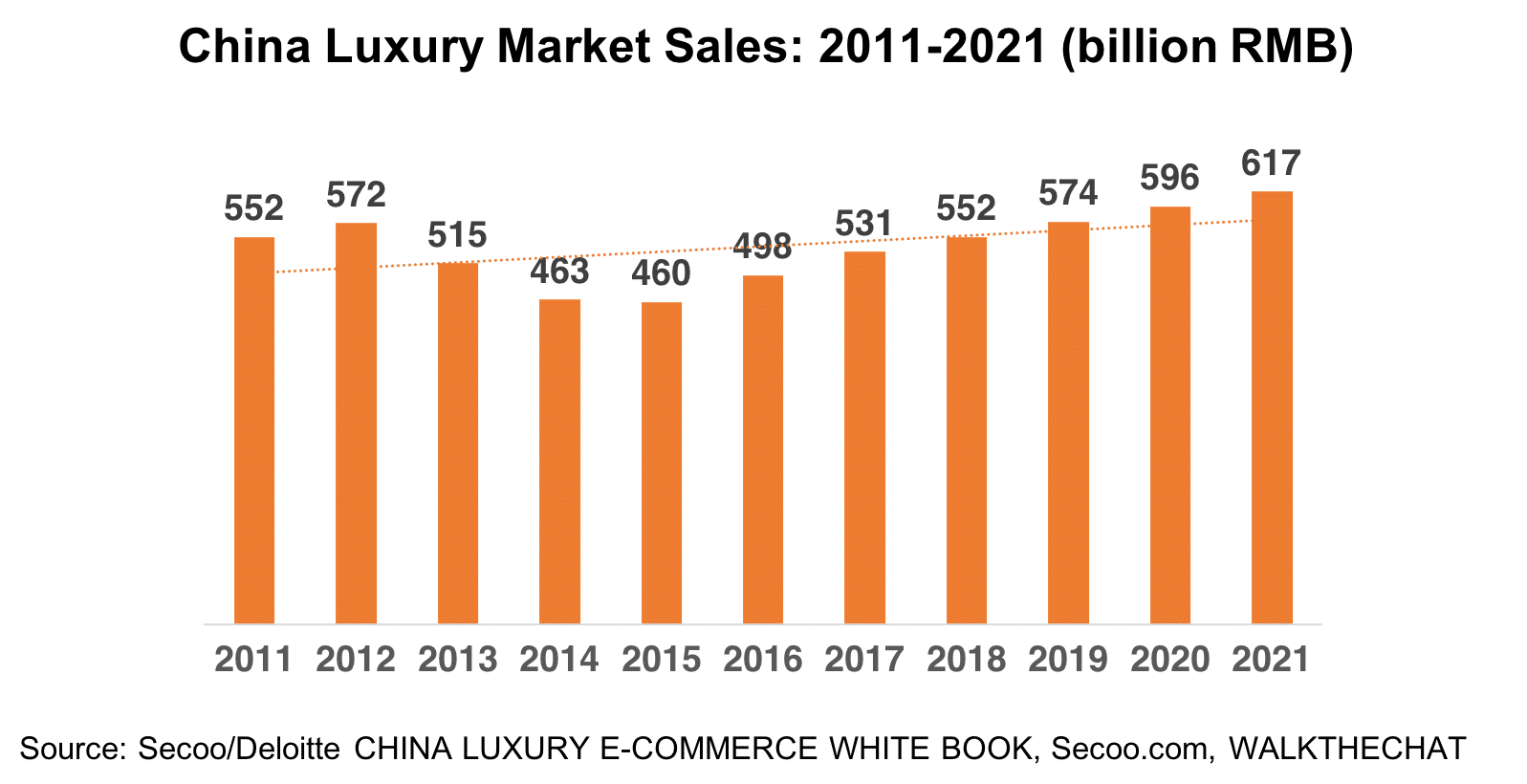

Back in 2018, we put together the best of luxury reports from McKinsey, Bain, Deloitte, Secoo and more in order to give you the best insights about the Digital Luxury Market in China.

Here’s a recap of last year’s luxury data!

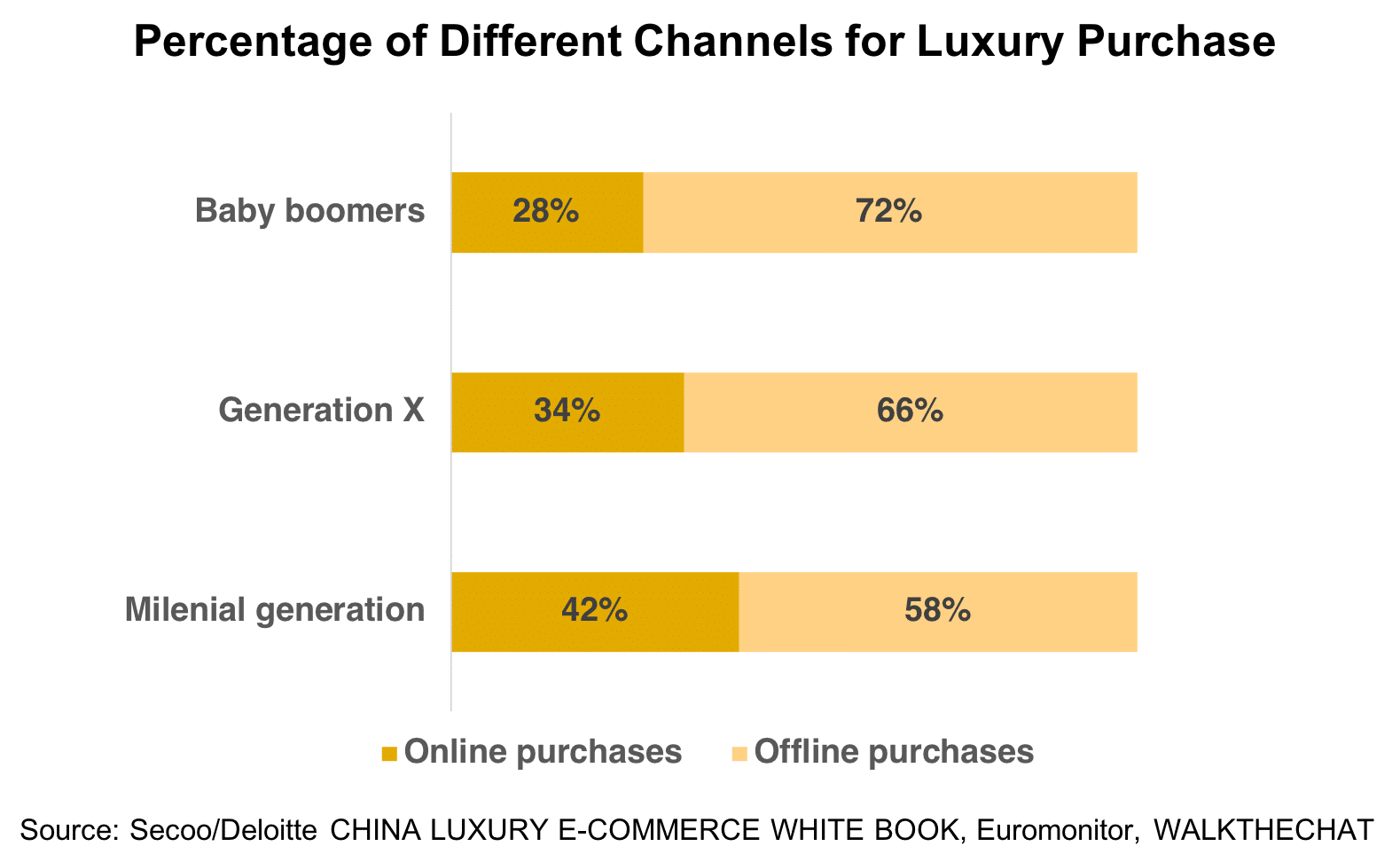

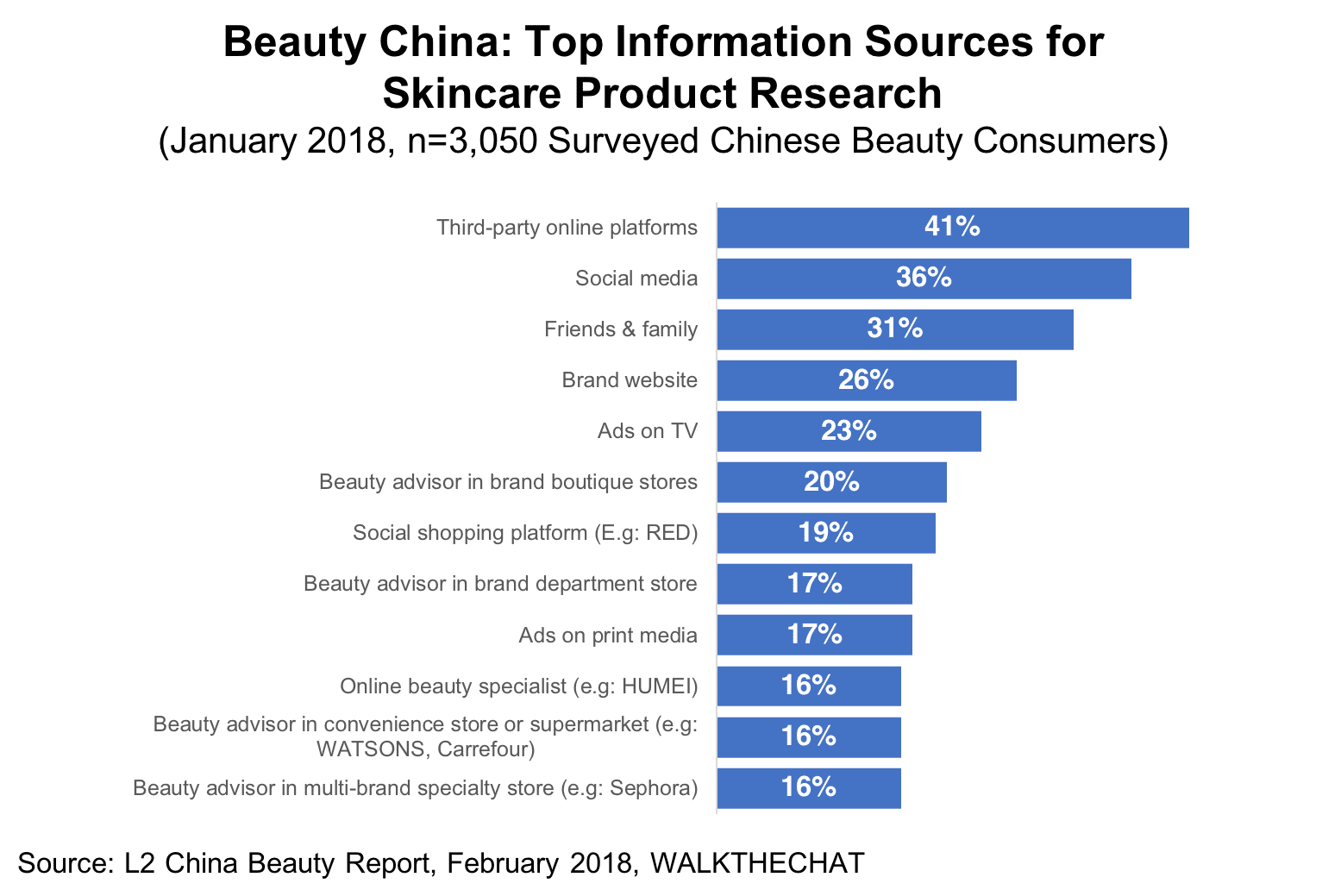

Millennial generation is more likely to purchase luxury products online: 42% would prefer buying online vs 58% will purchase in-store. In a survey with 240 consumers, 35.6% of consumers would purchase luxury products online. Most consumers choose to purchase luxury goods online due to more product choice, convenience, and flexibility of ordering time. McKinsey survey indicates 70% of luxury goods purchase is influenced by online.

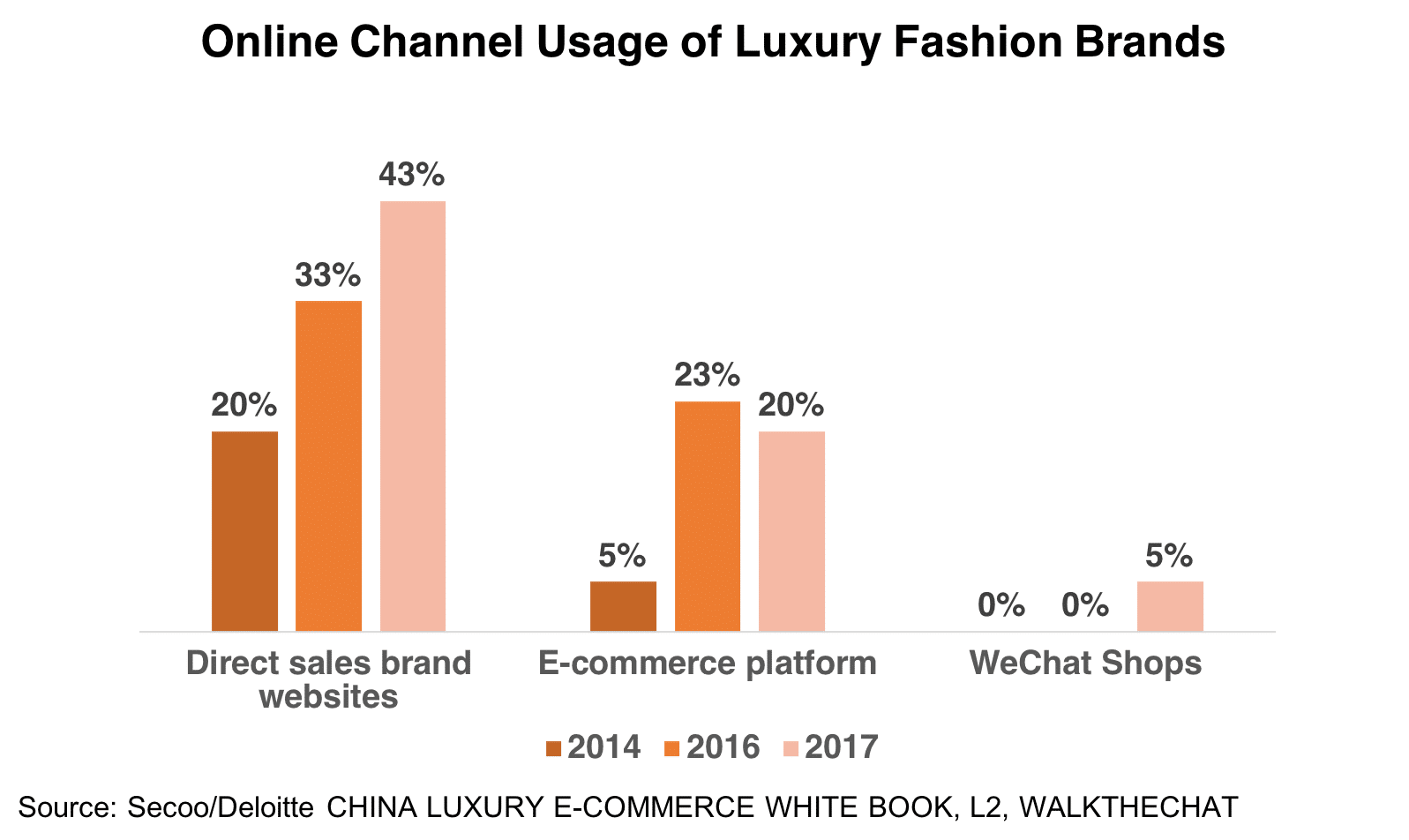

WeChat shops is becoming the major sales channel for luxury fashion brands, 5% of sales comes from WeChat in 2017.

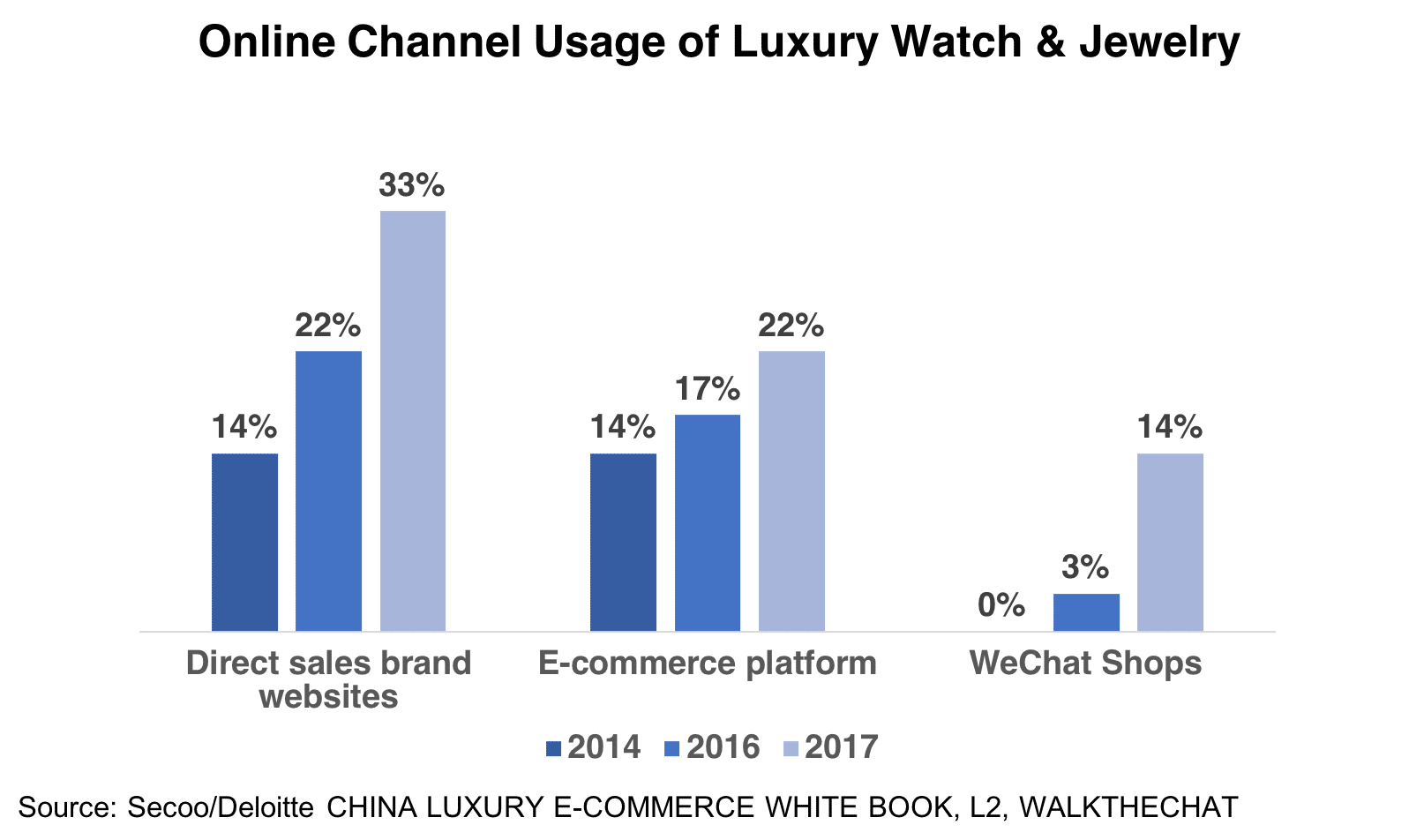

WeChat is a particularly important channel for luxury watch and jewelry industry. 14% of sales are coming from WeChat, and it will continue to grow.

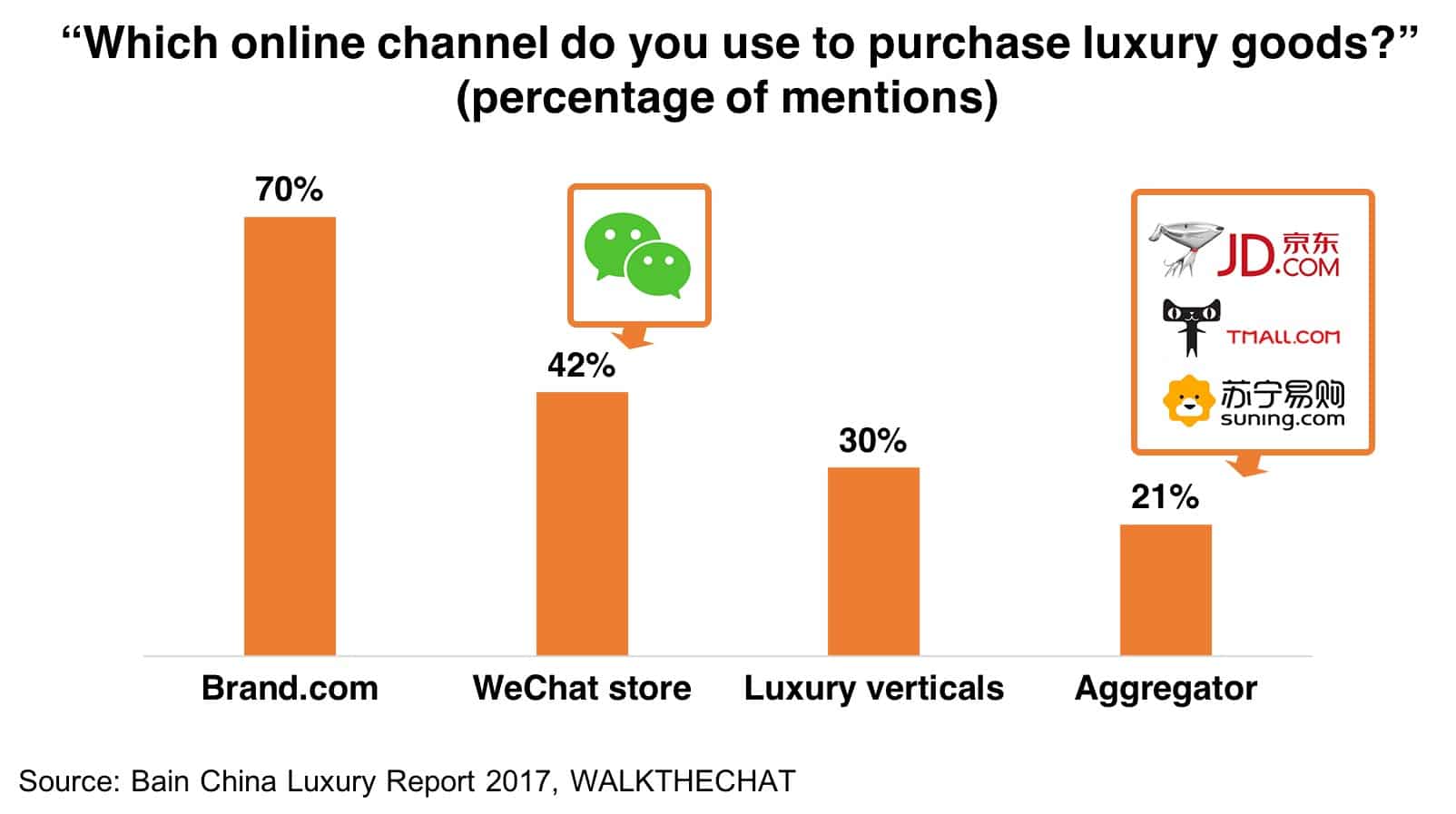

WeChat is a more popular channel for buying luxury goods than aggregators such as JD.com and Tmall. 42% consumers would buy luxury goods on WeChat, and only 21% will buy from aggregators.

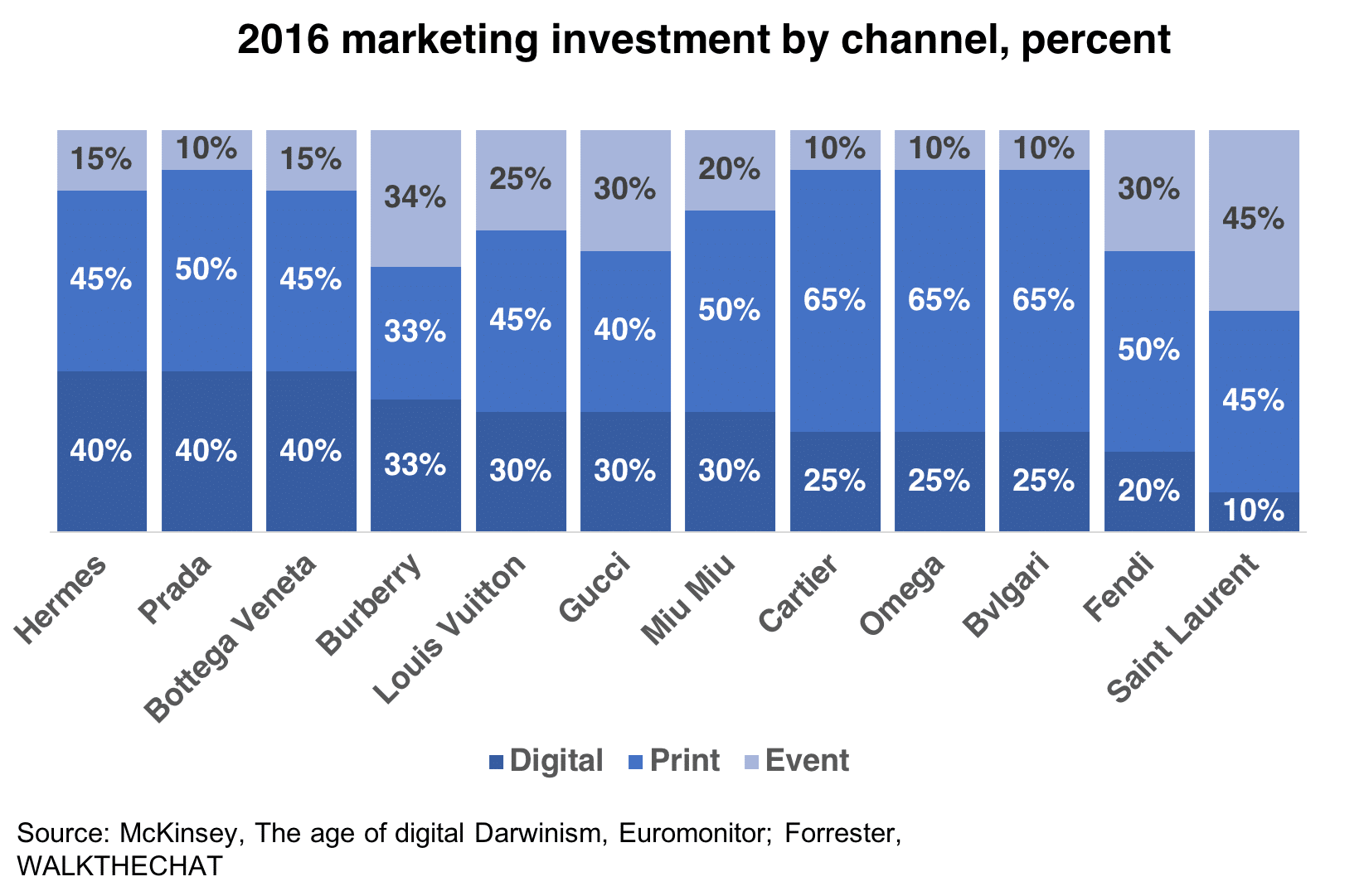

China is ranked #5 as the most popular country for luxury product sale. As of 2016, most luxury brands invest between 40%-10% of budget into digital marketing.

Elevate your China Marketing with AI-Driven Analytics and Creativity. Let's Talk.

The way consumers discover brands also depends on their age. The post-90s generations are much more likely to be experimental and go for up-and-coming brands, while older generations are loyal to a few brands they keep buying from.

The way consumers discover brands also depends on their age. The post-90s generations are much more likely to be experimental and go for up-and-coming brands, while older generations are loyal to a few brands they keep buying from.

Younger customers are also much more likely to engage in impulse purchases. 34% of 80s/90s generations will make their purchasing decisions in less than 3 days, against only 2% of post 65s/70s generation.

Younger customers are also much more likely to engage in impulse purchases. 34% of 80s/90s generations will make their purchasing decisions in less than 3 days, against only 2% of post 65s/70s generation.

However, purchasing behaviors are more complex: according to the BCG x Tencent report, 58% of luxury buyers purchase offline after having researched products online, while only 28% make purchases solely based on offline information.

This concept of online research to buy in offline stores is abbreviated as ROPO (Research Online, Purchase Offline) which is the opposite of showrooming (Research Offline, Purchase Online).

However, purchasing behaviors are more complex: according to the BCG x Tencent report, 58% of luxury buyers purchase offline after having researched products online, while only 28% make purchases solely based on offline information.

This concept of online research to buy in offline stores is abbreviated as ROPO (Research Online, Purchase Offline) which is the opposite of showrooming (Research Offline, Purchase Online).

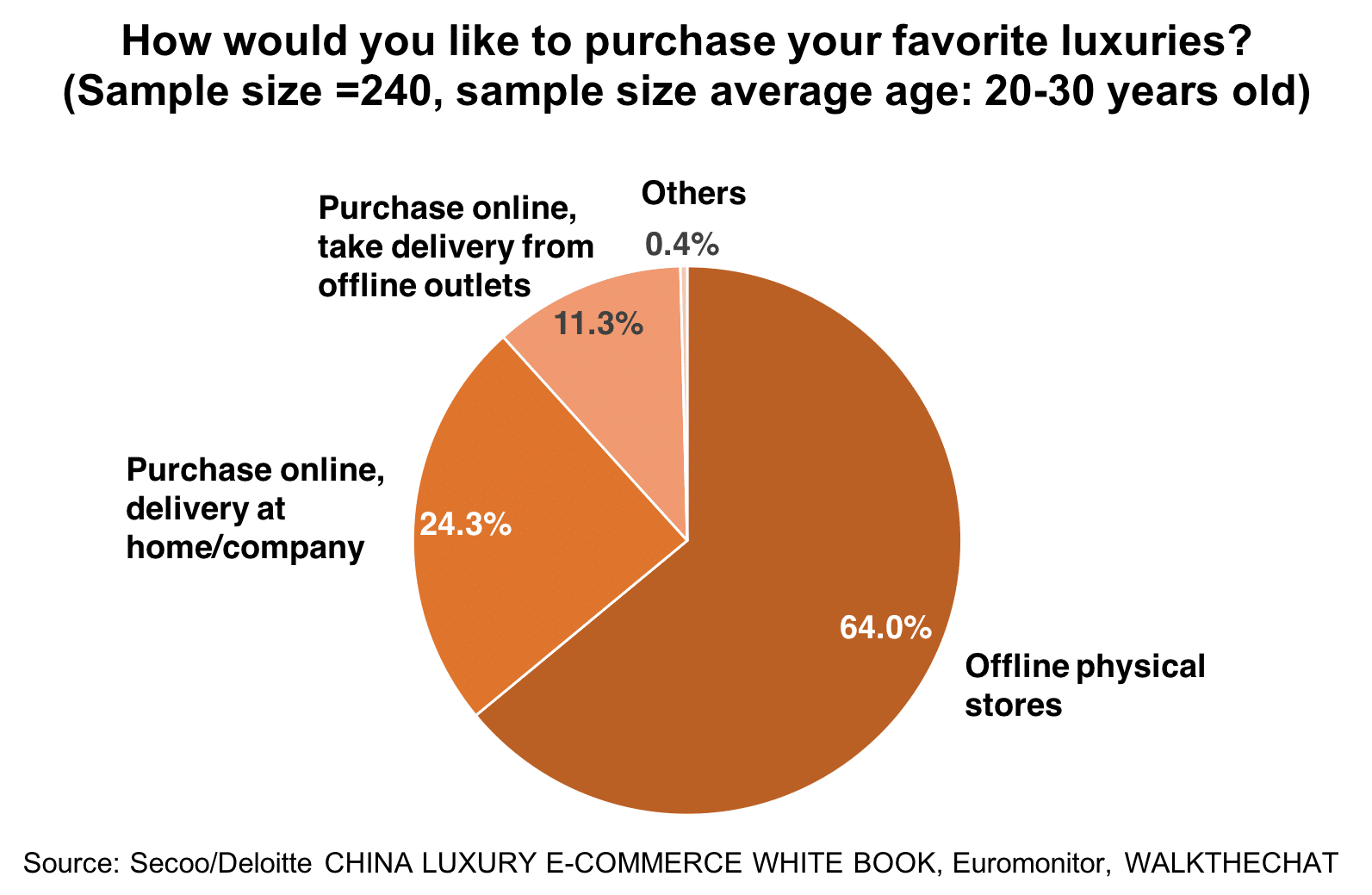

In a survey with 240 consumers, 35.6% of consumers would purchase luxury products online.

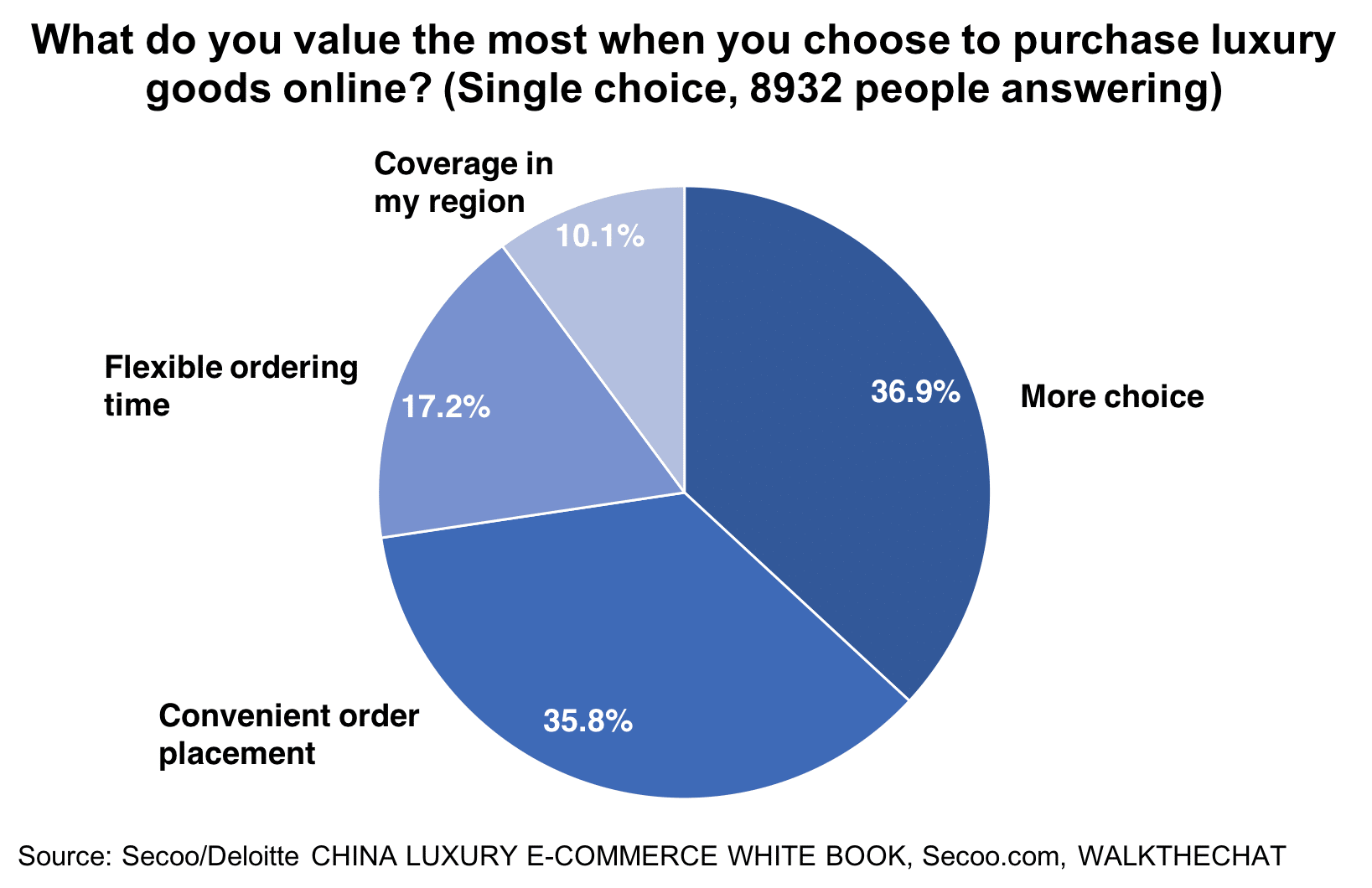

In a survey with 240 consumers, 35.6% of consumers would purchase luxury products online.  Most consumers choose to purchase luxury goods online due to more product choice, convenience, and flexibility of ordering time.

Most consumers choose to purchase luxury goods online due to more product choice, convenience, and flexibility of ordering time.  McKinsey survey indicates 70% of luxury goods purchase is influenced by online.

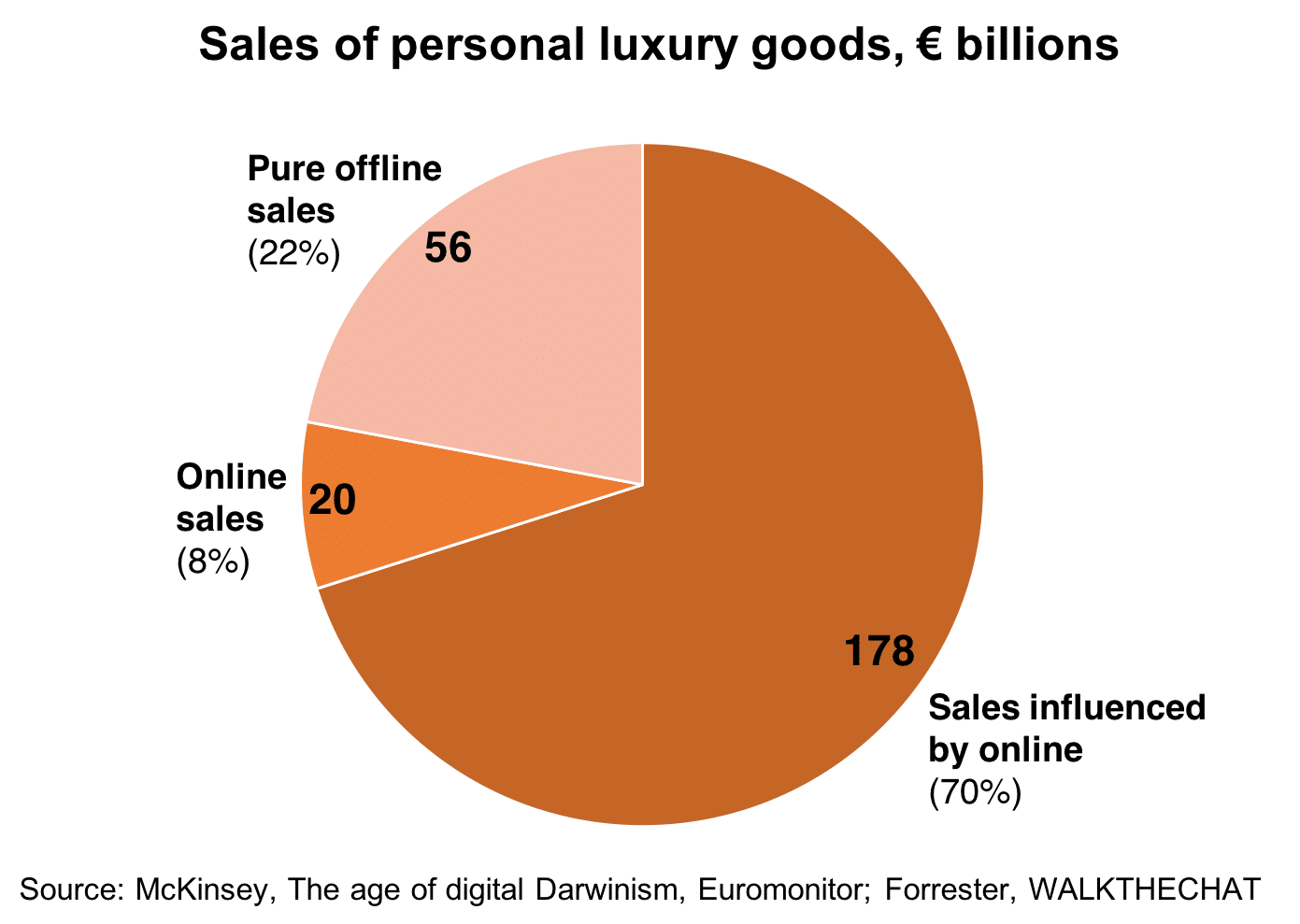

McKinsey survey indicates 70% of luxury goods purchase is influenced by online.

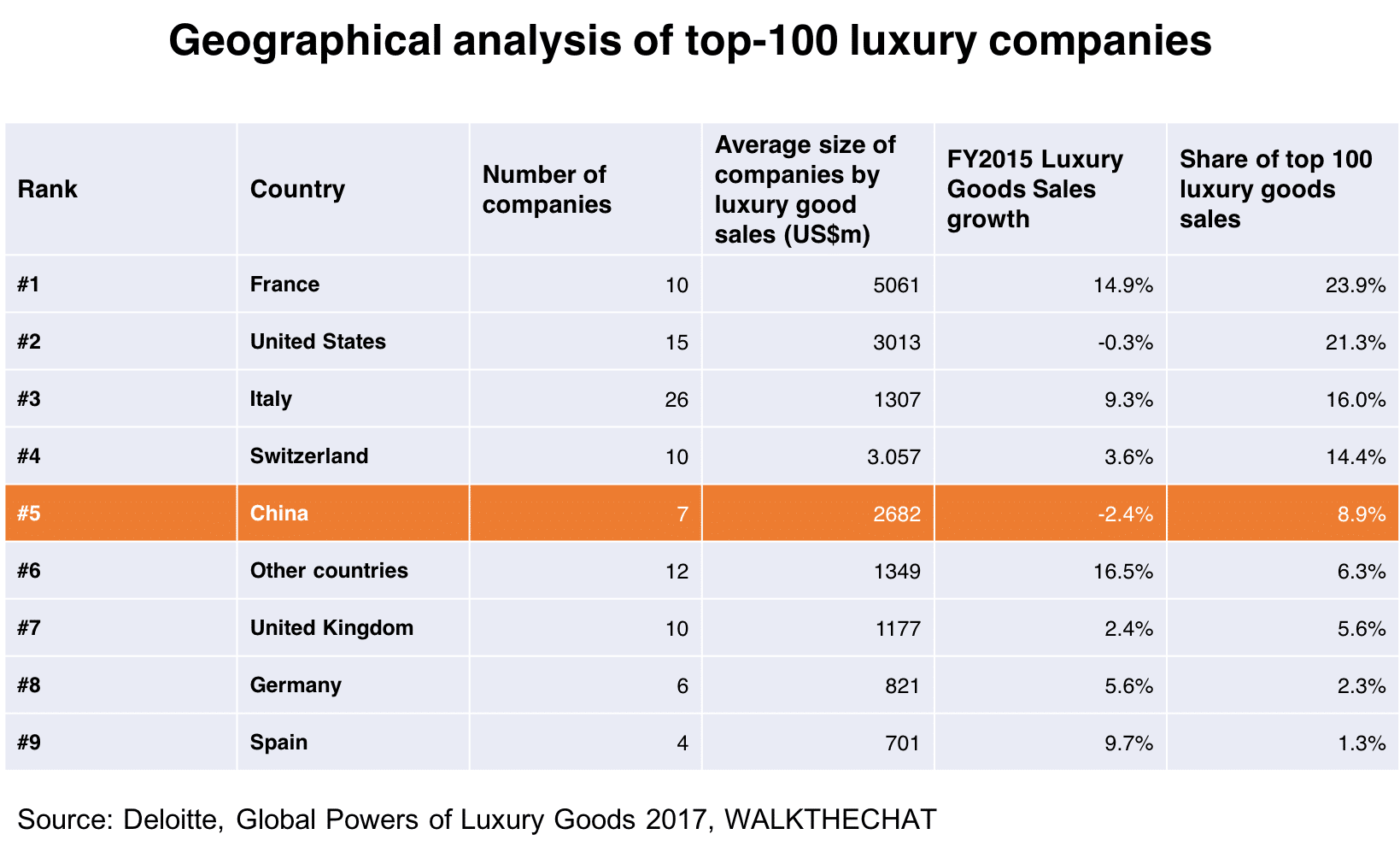

China is ranked #5 as the most popular country for luxury product sale.

China is ranked #5 as the most popular country for luxury product sale.  As of 2016, most luxury brands invest between 40%-10% of budget into digital marketing.

As of 2016, most luxury brands invest between 40%-10% of budget into digital marketing.